This spotlight is part of a series of deep-dive previews produced ahead of the upcoming State of RWAfi report, developed in collaboration with DefiLlama. The full report delivers a comprehensive, data-led assessment of the real-world asset landscape across DeFi, covering tokenised equities, real estate, commodities, and the broader structural forces shaping the next phase of onchain capital markets. The State of RWAfi Q1 2025 report will be published in the first week of April 2026.

Private credit has been one of the most talked-about asset classes when it comes to tokenisation, and for good reason. What has historically been an illiquid and hard-to-access asset class for retail investors is now being brought onchain and made liquid with much lower barriers to entry.

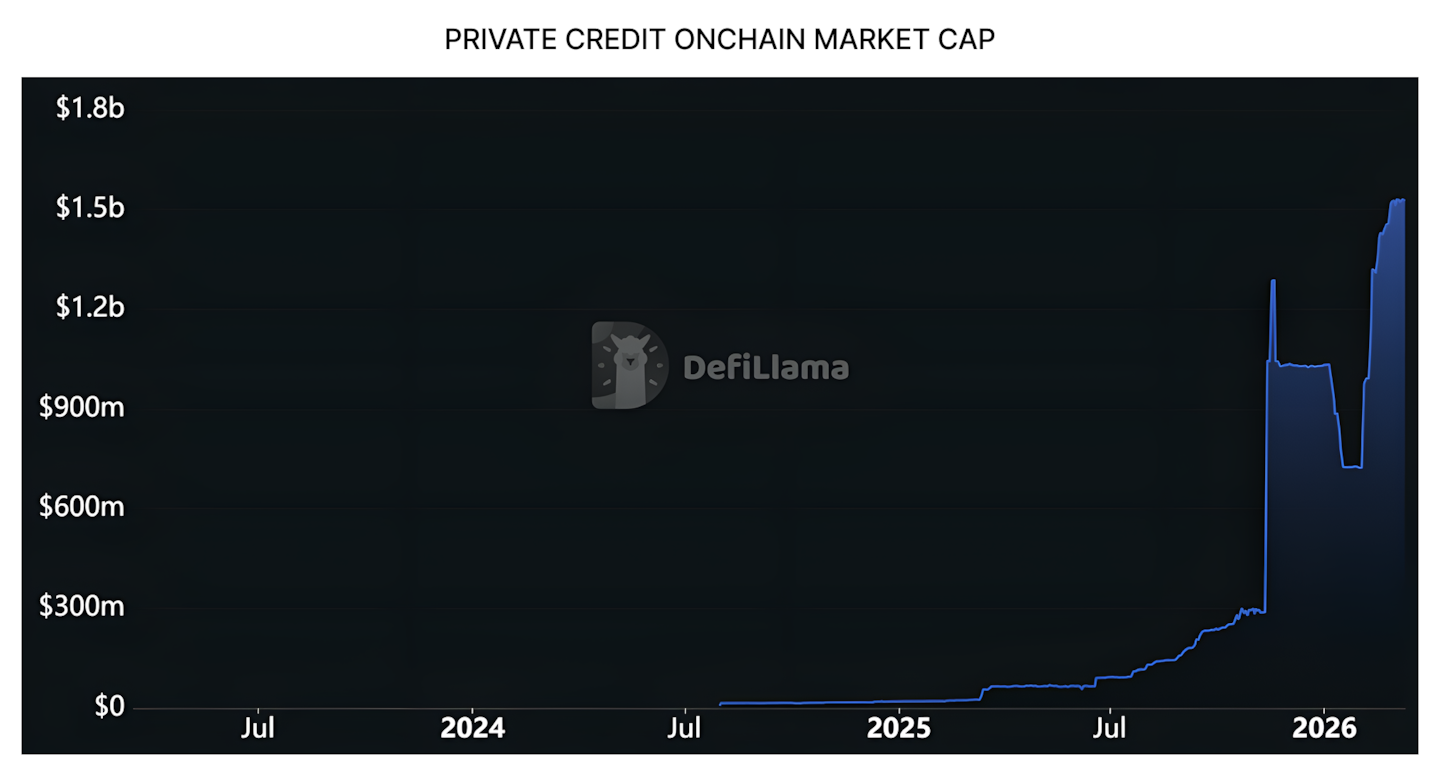

The growth of the sector over the past year underscores the rapid pace of this shift. In March 2025, the onchain market cap of private credit was only around $25 million. At the time of writing, however, the onchain market cap has expanded to $1.675 billion.

What is private credit, and why is it important?

To understand the significance of bringing private credit onchain, it is important to first understand what private credit actually is, how it developed, and the size of the existing market.

What private credit actually is

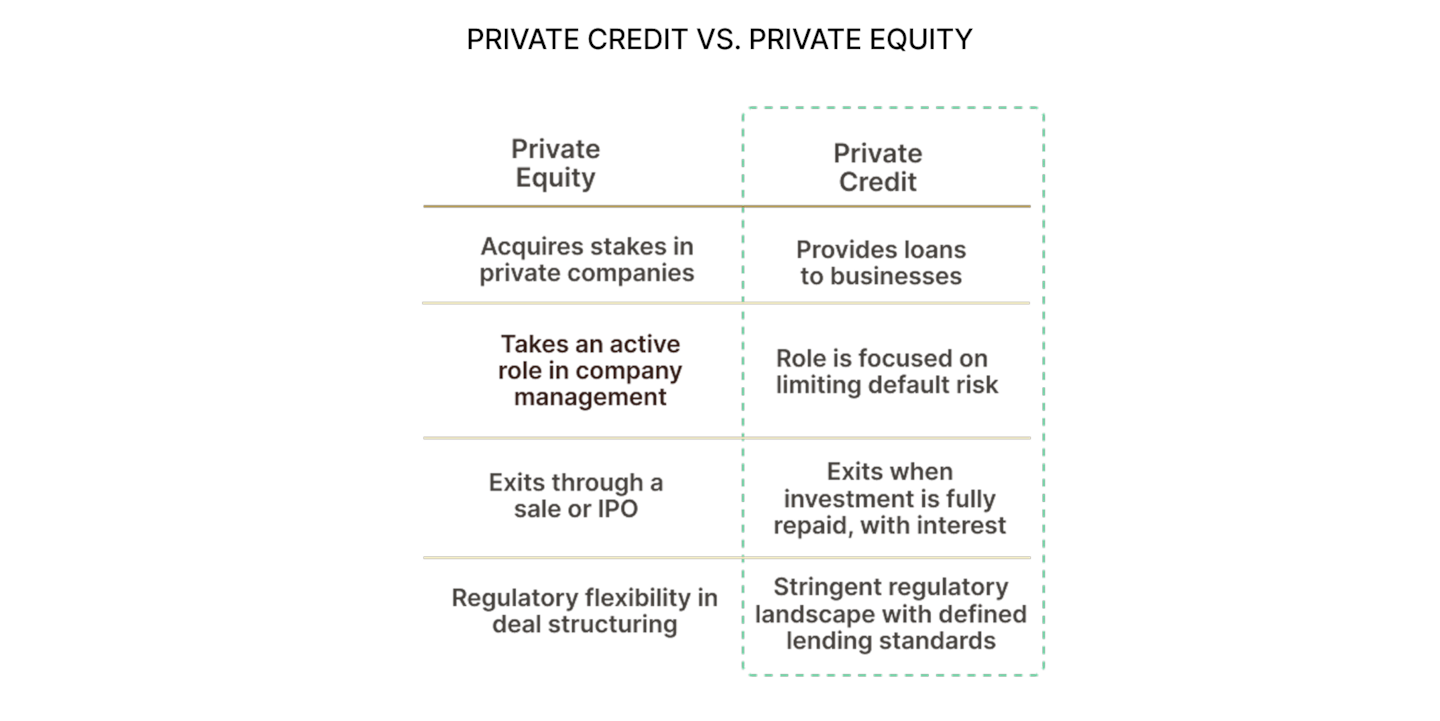

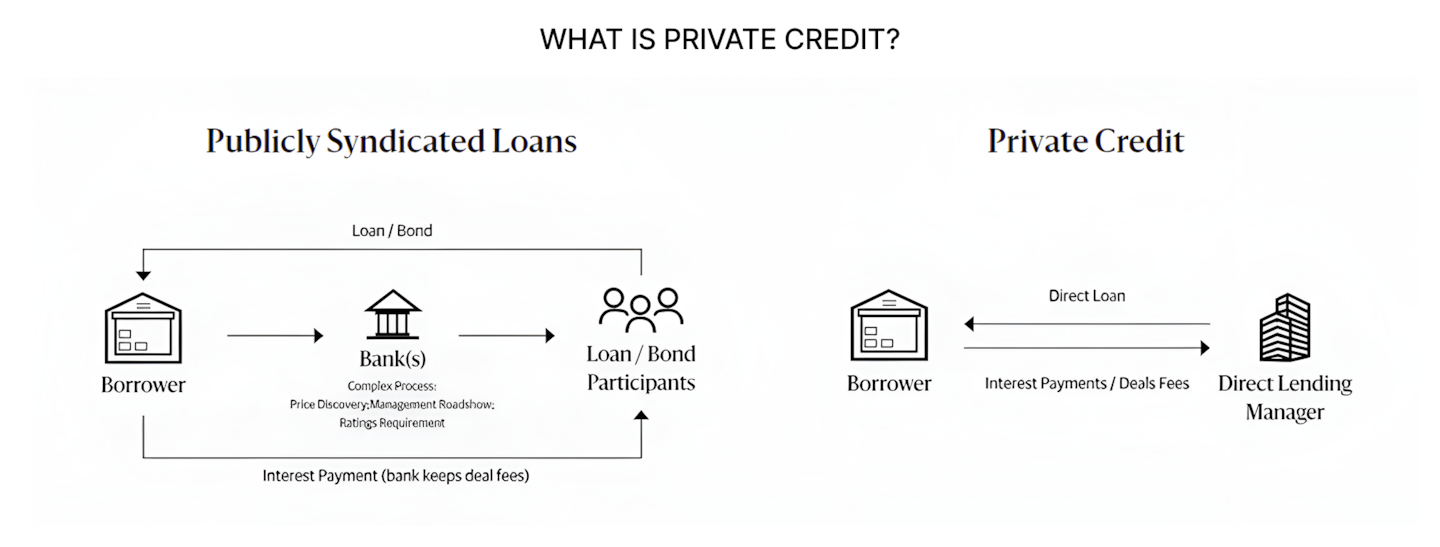

Private credit generally means lending by nonbank institutions outside public debt markets. Said another way, instead of raising money through a broadly syndicated loan or a public bond issuance, borrowers receive financing directly from private lenders such as credit funds, business development companies, insurers, and other alternative asset managers.

The market has historically focused on middle-market companies, but over time, it has expanded well beyond that niche.

In practice, private credit is often associated most closely with direct lending, and for good reason. With these transactions, a private lender or a small group of lenders negotiates directly with a borrower and provides a tailored loan, often with floating rates and senior secured terms.

But private credit is broader than direct lending alone. It also includes strategies such as mezzanine debt, distressed debt, special situations, venture debt, infrastructure debt, and other forms of bespoke financing

How private credit became so popular

One of the most important drivers was the retrenchment of banks. After 2008, tighter regulation and changes in bank capital treatment increased the capital and balance-sheet costs of holding certain types of leveraged and middle-market loans, making them less attractive for banks to retain on their balance sheets.

This created a gap in the market, especially for borrowers who still needed flexible financing but could no longer rely as easily on traditional bank lending. Private lenders stepped in to fill that gap.

At the same time, private equity was growing rapidly and needed financing solutions that were faster, more tailored, and often more flexible than syndicated loan markets could provide. This created a natural link between private equity and private credit.

Investor demand also played a major role. In a low-rate world, institutional investors were looking for higher-yielding private market exposure. Private credit offered exactly that, often combined with floating-rate structures and senior secured positioning in the capital structure. As the market matured, it also became more attractive because lenders themselves became better capitalised and more competitive.

Taken together, these forces turned private credit from a niche alternative strategy into one of the fastest-growing parts of the private market.

How large is the private credit market today?

Private credit is now a market of real scale, but its exact size depends on how it is measured. Some institutions define the market narrowly as private credit fund assets under management, while others use a broader definition that also includes undeployed capital commitments, often referred to as dry powder.

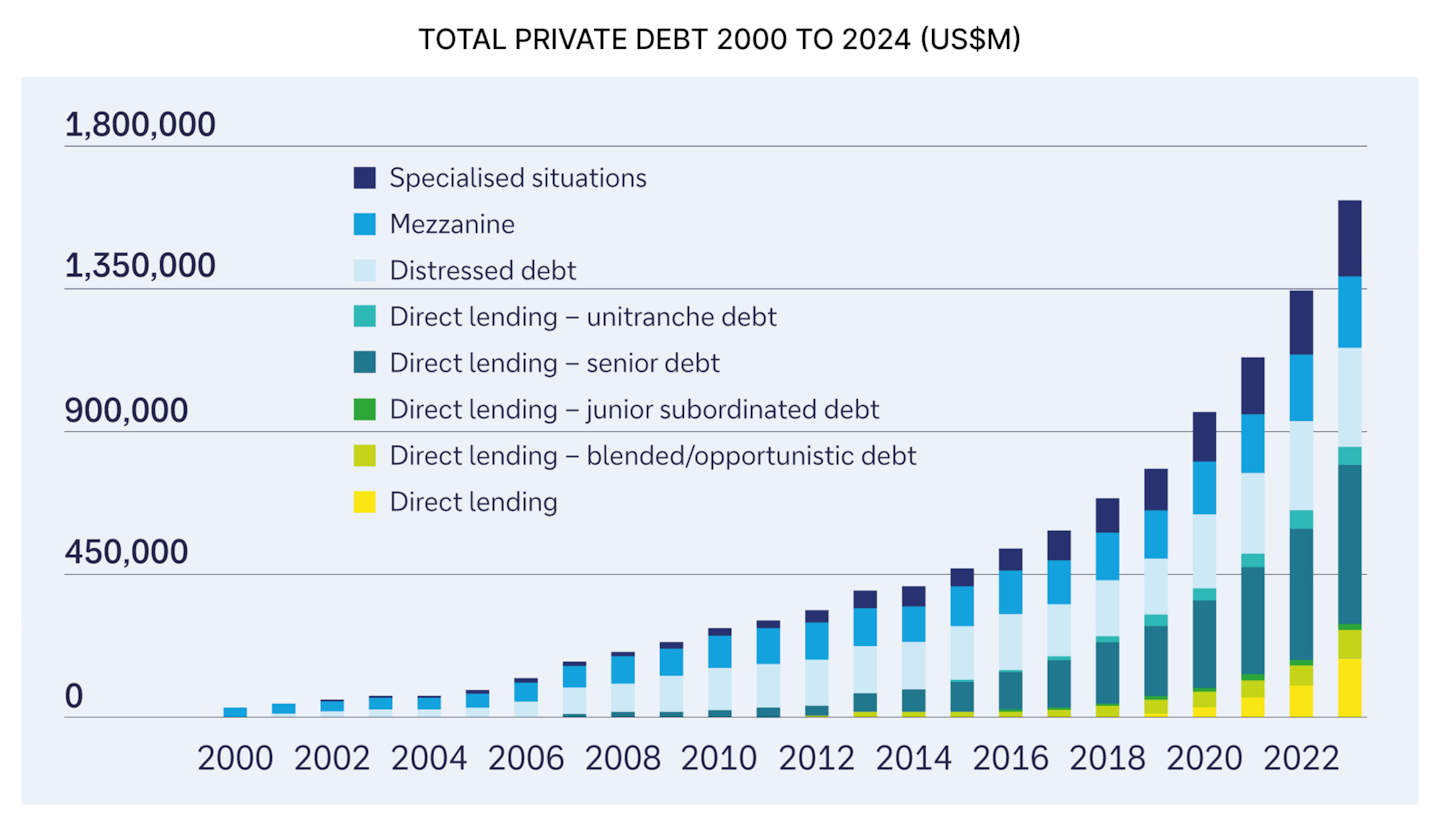

The Federal Reserve estimates that private credit totaled $1.34 trillion in the United States and nearly $2 trillion globally by the second quarter of 2024, having grown roughly five times since 2009.

Broader industry measures put the market higher. In December 2025, the Alternative Credit Council reported that global private credit had reached $3.5 trillion in assets under management, with $592.8 billion deployed in 2024 alone

These differences in market size are largely methodological. Narrower estimates focus on the core private credit market as it is most commonly measured by policymakers and central banks. Broader estimates capture a wider universe of strategies, vehicles, and undeployed capital across the private credit ecosystem.

What is clear, however, is that the total addressable market for tokenisation is substantial, and private credit has grown rapidly since 2008.

Why tokenise private credit?

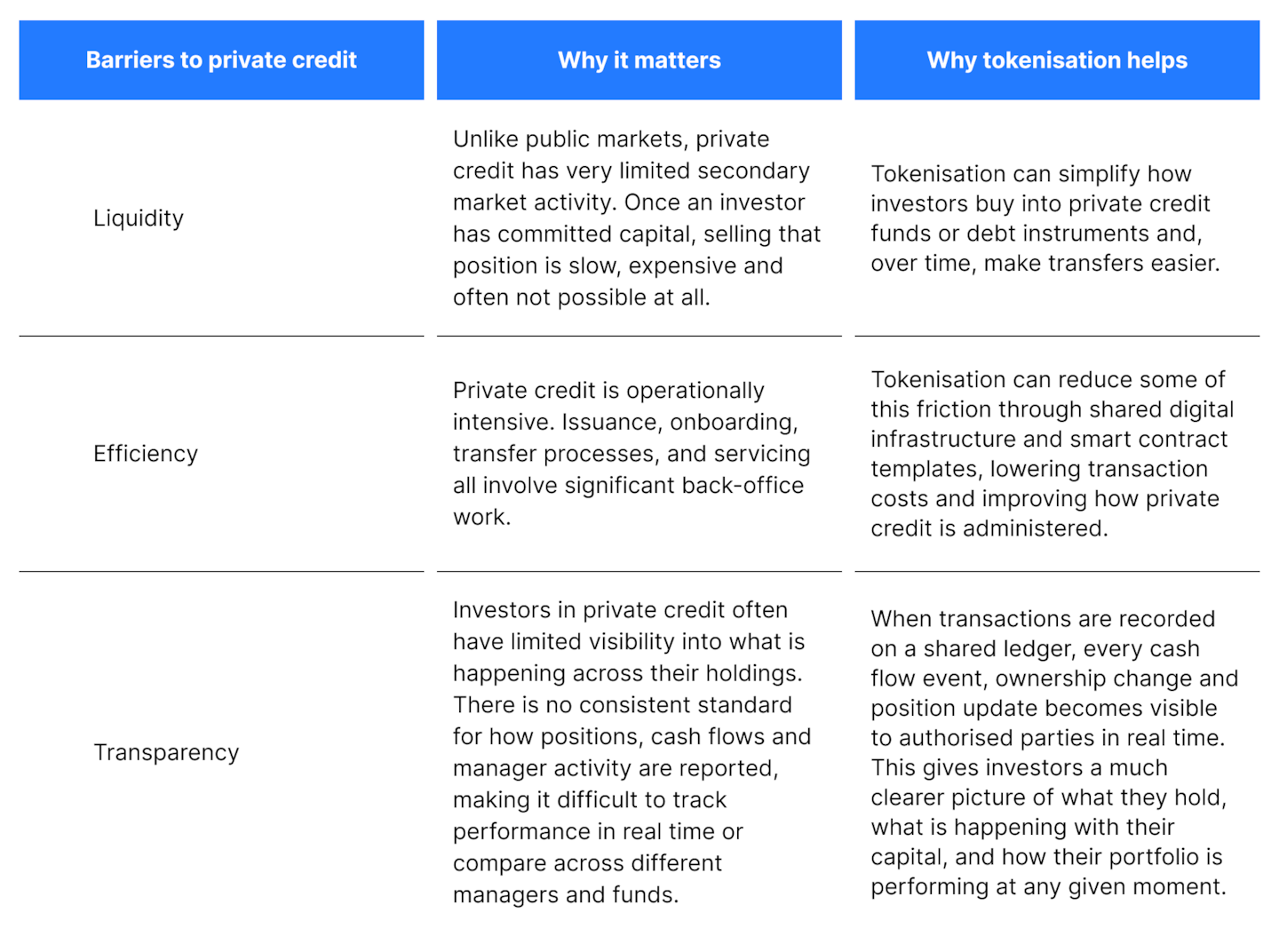

While private credit has grown into a multi-trillion-dollar market, it still carries many of the frictions associated with private assets. Access remains limited, transfers are often cumbersome, reporting is less standardised than in public markets, and the market remains operationally heavy for both managers and investors.

One of the clearest ways to frame these challenges, and how tokenisation may help address them, is by focusing on three key barriers: liquidity, efficiency, and transparency.

Taken together, these three barriers point to a consistent underlying problem. Private credit has scaled rapidly as an asset class, but the infrastructure supporting it has not kept pace. The market still relies heavily on bilateral processes, fragmented systems and manual oversight that were designed for a much smaller and more concentrated investor base. As the asset class continues to grow and attract a broader range of participants, those structural limitations become harder to absorb.

Rather than addressing each friction in isolation, a shared digital infrastructure has the potential to resolve all three simultaneously. Liquidity improves when ownership can be transferred digitally. Efficiency improves when issuance and servicing run on common rails. Transparency improves when every transaction is recorded on a single ledger visible to all authorised parties. The value of tokenisation in private credit is not that it does any one of these things particularly well. It is that it can do all of them within the same architecture.

That potential has not gone unnoticed. A growing number of asset managers, banks and technology platforms have begun building towards exactly this kind of infrastructure, and the market for tokenised private credit is developing quickly.

The types of tokenised private credit and the main players

Not all tokenised private credit is structured in the same way. The market has developed along several distinct models, each reflecting a different approach to how credit is originated, packaged and made available to investors onchain.

Based on the assets tracked by DeFiLlama, four main types have emerged: tokenised private credit funds, onchain lending pools, structured and speciality credit, and reinsurance-linked credit.

Tokenised private credit funds

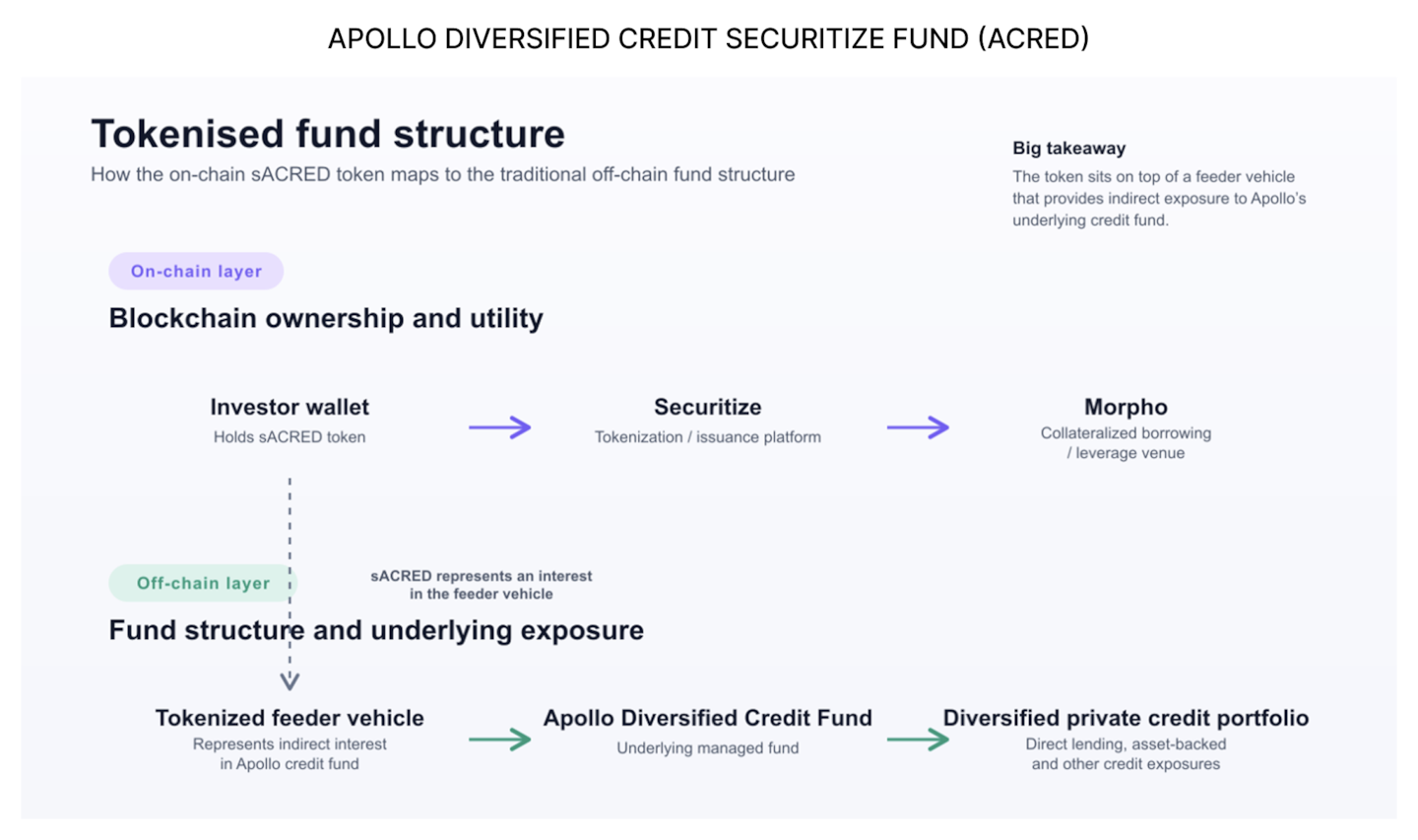

The most recognisable category is the tokenised private credit fund. In this model, the underlying credit strategy remains a conventional private credit fund managed offchain, while the ownership layer is brought onchain through a tokenised feeder vehicle or similar wrapper.

To make that structure more concrete, it is useful to look at Apollo’s ACRED architecture. The visual shows the model in layers. At the foundation sits Apollo’s Diversified Credit Fund and the underlying portfolio of private credit assets. Above that sits the feeder structure through which investors gain exposure.

Only then does the onchain layer appear, with Securitize handling the tokenised ownership record and the ACRED token sitting in the investor’s wallet. From there, the token can plug into onchain venues such as Morpho.

That is the key point of this model. The blockchain does not replace the underlying fund. It sits above it and changes how ownership is recorded, transferred, and potentially used. For managers, that makes tokenisation an easier starting point because it does not require them to rebuild origination, underwriting, or servicing. For investors, it can make access and transfer simpler, even if the underlying assets remain illiquid.

The main benefit of tokenisation is distribution.

Private credit funds have historically been difficult to access and operationally cumbersome to transfer. Tokenisation does not solve the liquidity of the loans themselves, but it can make the ownership layer easier to manage and more compatible with digital financial infrastructure.

Who are the key players?

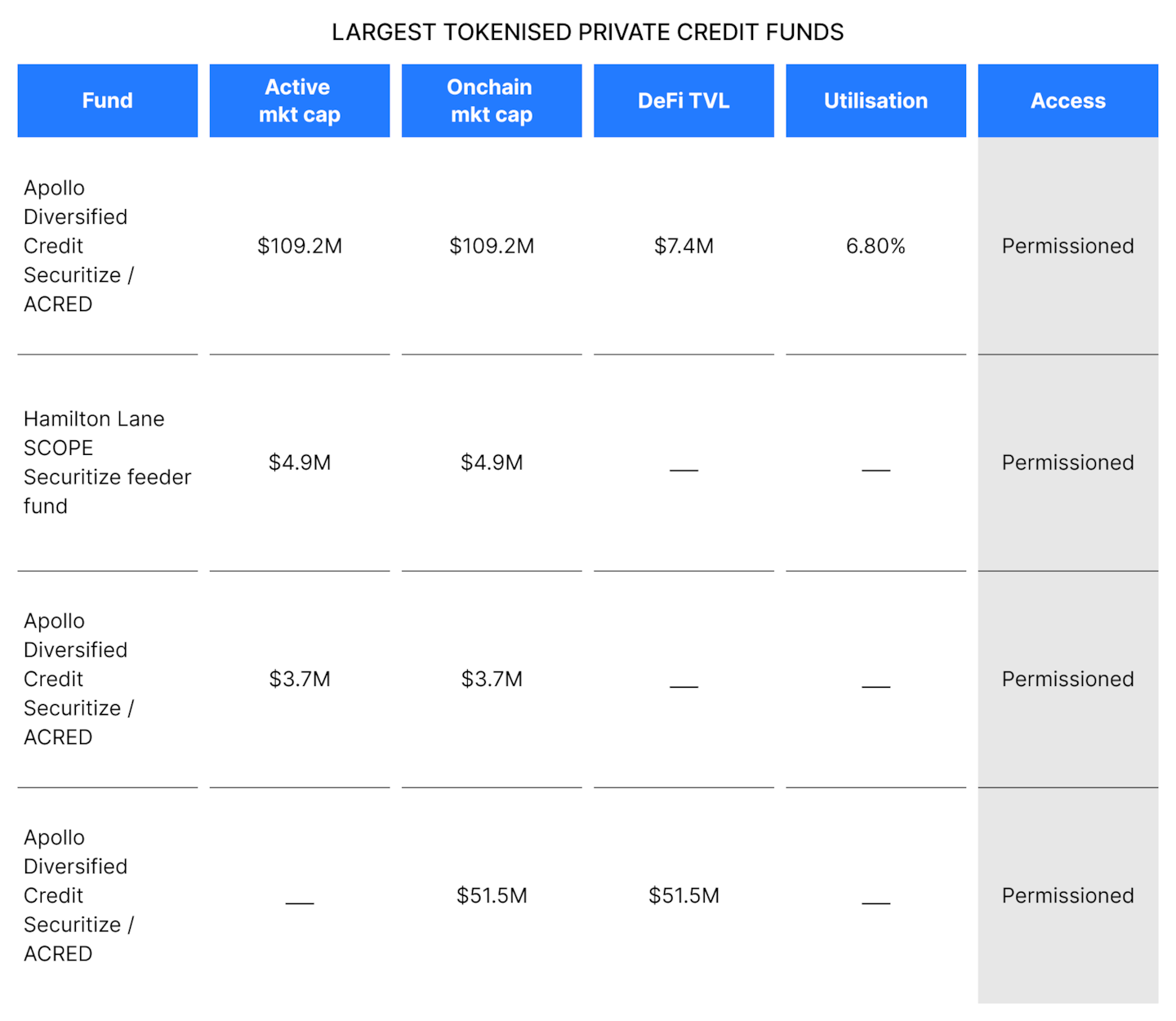

Apollo’s ACRED is the largest named product by active market cap at $109.2 million, which puts it comfortably ahead of Hamilton Lane SCOPE at $4.9 million and WisdomTree’s Private Credit Digital Fund at $3.7 million.

Anemoy’s tokenised Apollo exposure also stands out with $51.5 million of onchain market cap, reinforcing the point that Apollo-linked exposure is currently the most scaled strategy in this part of the market.

The common denominator among the leaders is fairly clear. They are all tied to recognised managers or institutional distribution networks, and they all sit inside permissioned structures. That matters. In the fund segment, investors are not selecting these products because they are the most DeFi-native. They are selecting them because the manager is credible, the product is familiar, and the wrapper makes an otherwise hard-to-access strategy easier to hold.

The winners here are therefore the managers with the strongest brand, the clearest institutional distribution story, and a product that can be brought onchain without changing its core investment process.

Onchain lending pools

Onchain lending pools take a more direct approach. Rather than tokenising access to an existing fund, they place the lending activity itself into blockchain infrastructure.

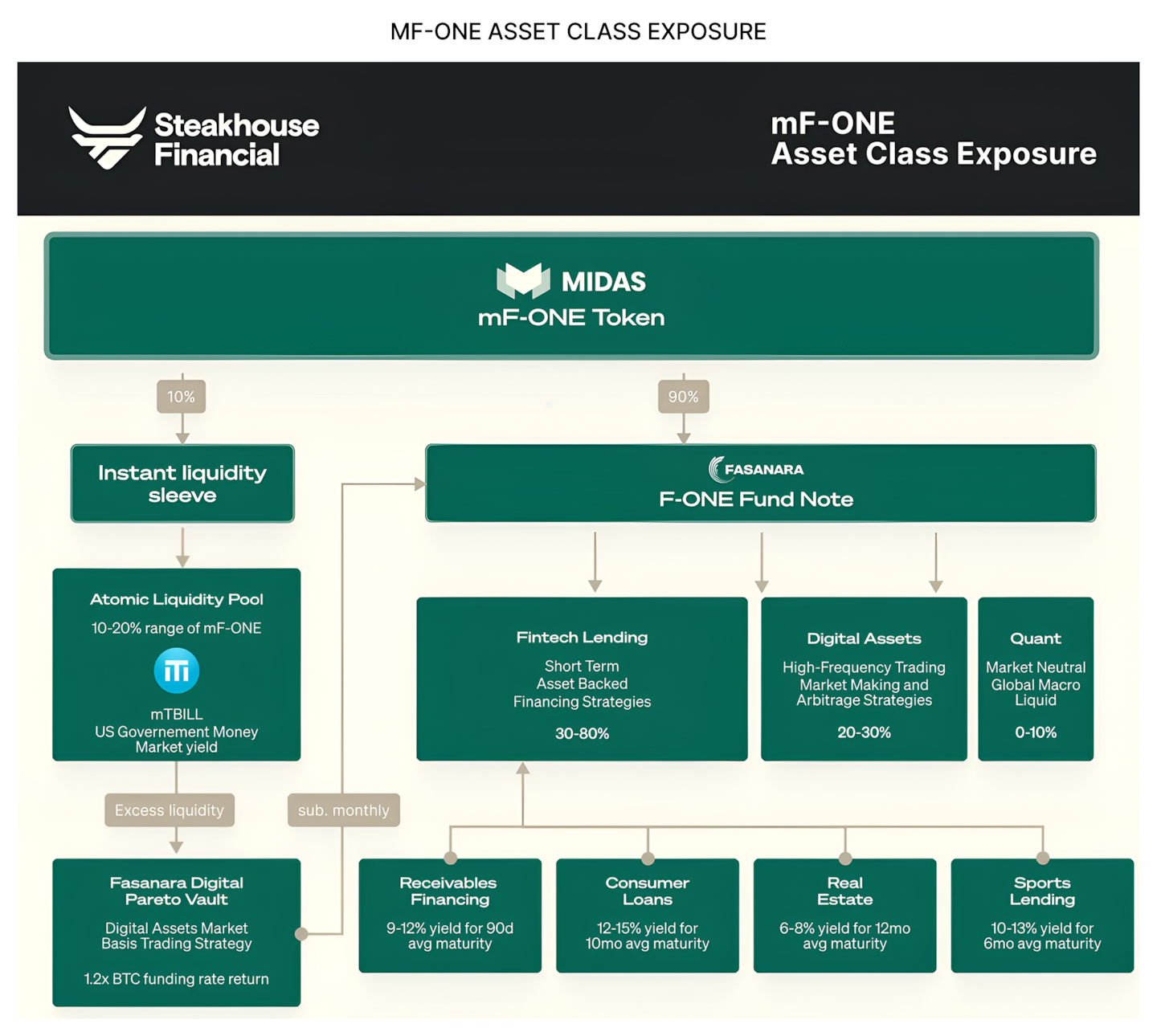

The architecture of mF-ONE helps illustrate how this works in practice. The structure begins with the onchain token that investors hold. Beneath that sits the fund note and liquidity sleeve that connect the token to the underlying portfolio. That portfolio is then allocated across a range of lending strategies, including fintech lending, digital asset credit, and quantitative strategies, which in turn map to more specific exposures such as receivables financing, consumer loans, real estate, and sports lending.

Seen this way, the token is the entry point, but the economic exposure runs much deeper.

The investor holds a blockchain-native asset, while the credit risk underneath remains diversified across multiple real-world channels. That is what makes this category distinct from the tokenised fund model. It is designed to function more like a live onchain credit market, with capital pooled, deployed, and monitored through more visible onchain rails.

The reason the model has become popular among a specific set of institutional borrowers is straightforward. Crypto-native trading firms, fintechs and financial institutions that need short-term stablecoin liquidity can access capital through these protocols more flexibly than through traditional banking relationships, and they are willing to accept the visibility that comes with having their borrowing activity on a public blockchain.

For DeFi lenders, the appeal is yields that are typically higher than overcollateralised money markets can offer, in exchange for taking real credit risk on identifiable counterparties

Who are the key players?

The standout product here is mF-ONE, which combines the largest onchain market cap in the group at $98.8 million with $29.6 million in DeFi TVL and 95.0% utilisation. That makes it both the largest and the most actively used product in the category.

Clearpool TPOOL is the next-largest name by active market cap at $34.1 million, but its utilisation is only 5.7%, which makes it much less capital-efficient than mF-ONE. Nest Alpha Vault is smaller at $8.1 million, but its 82.4% utilisation is high enough to make it more operationally interesting than its size alone would suggest.

The products that lead are the ones with deeper deployment, stronger usage, and more visible integration into DeFi activity. That makes this segment very different from the tokenised fund market. Here, the winners are not simply the best-known names; they are the products that show they can actually put capital to work.

Structured and speciality credit

Structured and speciality credit is where tokenisation becomes more targeted. Rather than wrapping a broad private credit fund or lending pool, these products bring specific credit exposures onchain, such as CLO tranches, trade finance receivables, invoice pools, or structured notes.

That makes this category different from the others. Instead of buying into a general lending strategy, the investor is buying into a defined instrument with a clearer risk profile, a defined place in the capital structure, and a more predictable set of cash flows. In most cases, the assets sit inside an SPV, and the token represents a fractional interest in that vehicle. Cash flows from the underlying assets then flow back to tokenholders according to the rules of the structure.

This is also why structured and speciality credit is a natural fit for tokenisation. These products are already built around clearly defined claims and payment waterfalls. Tokenisation does not change the underlying exposure. It makes that exposure easier to package, distribute, and in some cases, integrate with onchain markets.

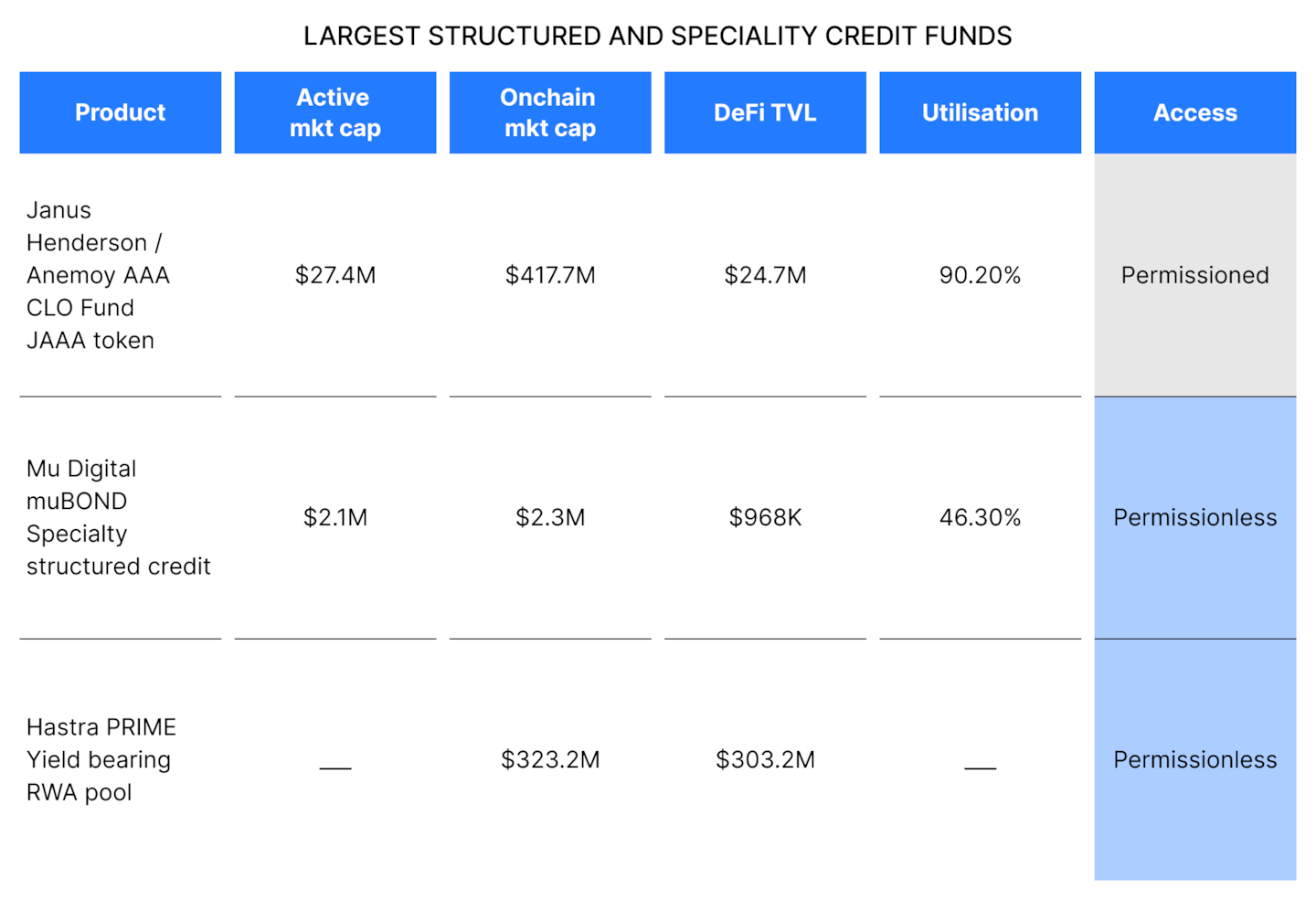

Who are the key players?

The leaders in this segment are Janus Henderson / Anemoy AAA CLO Fund and Hastra PRIME, and the gap to the rest of the field is already significant. Janus Henderson / Anemoy is the clearest institutional leader, with $417.7 million in onchain market cap and 90.2% utilisation. In comparison, Hastra PRIME follows with $323.2 million in onchain market cap and an exceptionally high $303.2 million in DeFi TVL.

By contrast, Mu Digital’s muBOND remains much smaller at $2.3 million in onchain market cap, which shows how concentrated this category still is:

What is interesting is that the two winners are not leading for the same reason. Janus Henderson / Anemoy stands out because it brings a highly recognisable structured credit product, a AAA CLO exposure, into a tokenised format that institutional investors can understand immediately. Hastra PRIME, by contrast, stands out because it appears to be much more deeply embedded in onchain finance, as shown by its very large DeFi TVL relative to its size. In other words, one leads through institutional familiarity, the other through onchain utility

Reinsurance-linked credit

Reinsurance-linked credit is the most conceptually distinct of the four types and needs to be understood on its own terms. This is not corporate credit. The investor is not lending to a company or buying a piece of a structured loan portfolio. They are providing capital to underwrite insurance and reinsurance risk, and in return, they receive premiums paid by primary insurers who want to transfer a portion of that risk off their own balance sheets.

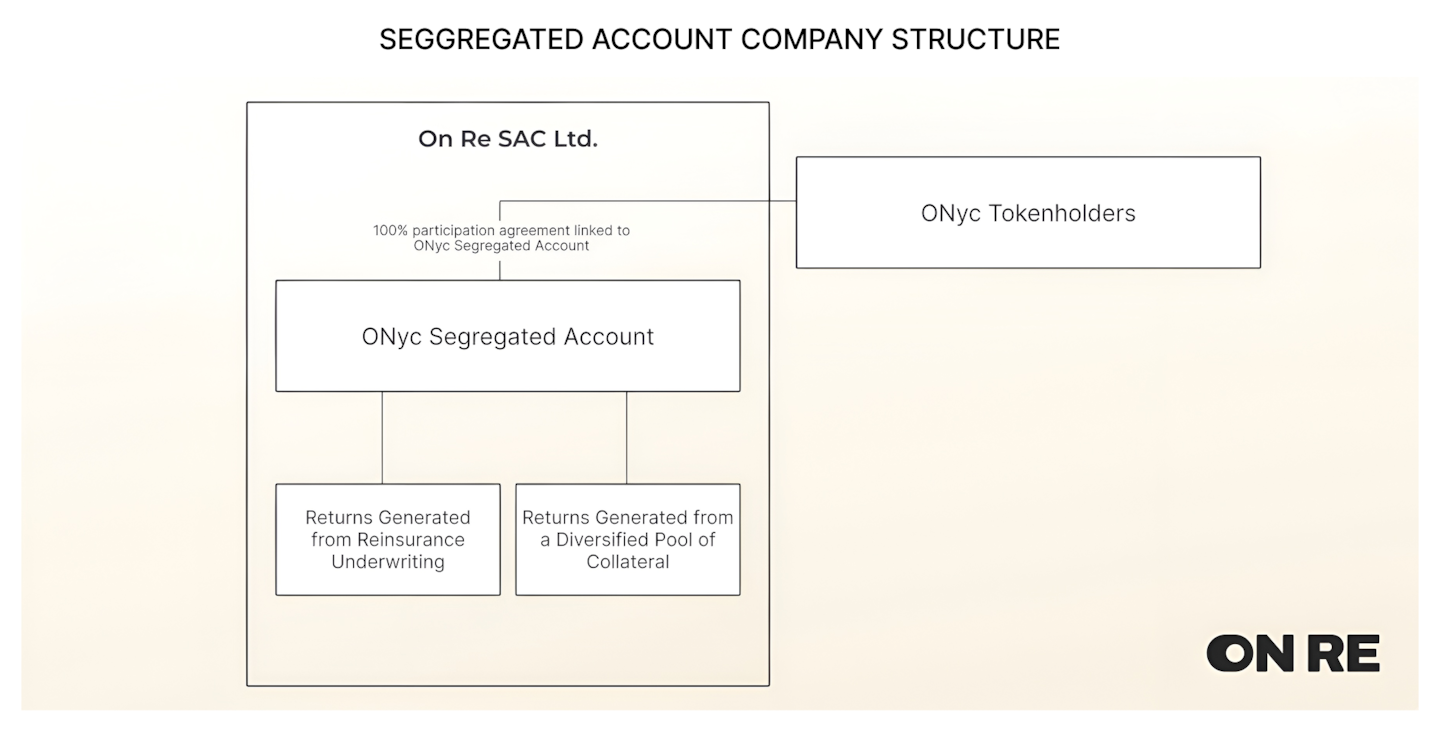

OnRe’s structure makes this easier to understand. The architecture shows tokenholders on one side and a ring-fenced capital structure on the other. Capital is allocated into a segregated account, and returns are generated from two linked sources: reinsurance underwriting income and the collateral pool that supports the structure. The token, therefore, represents exposure not to a conventional loan book, but to a specialist insurance-risk framework.

Understanding the reinsurance market itself is a prerequisite for understanding why tokenising it matters. Reinsurance is a large and well-established industry, with global reinsurance capital estimated at over $750 billion. It plays a critical role in allowing primary insurers to take on policies they could not otherwise hold given their own capital constraints, and it is an important mechanism through which catastrophic risk is distributed across the global financial system.

The uncorrelated nature of reinsurance returns has made insurance-linked securities attractive to institutional allocators for decades. What is new here is the accessibility. Before these products existed onchain, participating in reinsurance as an investor required either being a large institutional capital provider, an accredited investor in a specialist ILS fund, or a reinsurance company itself. A permissionless onchain structure removes most of those barriers.

Who are the key players?

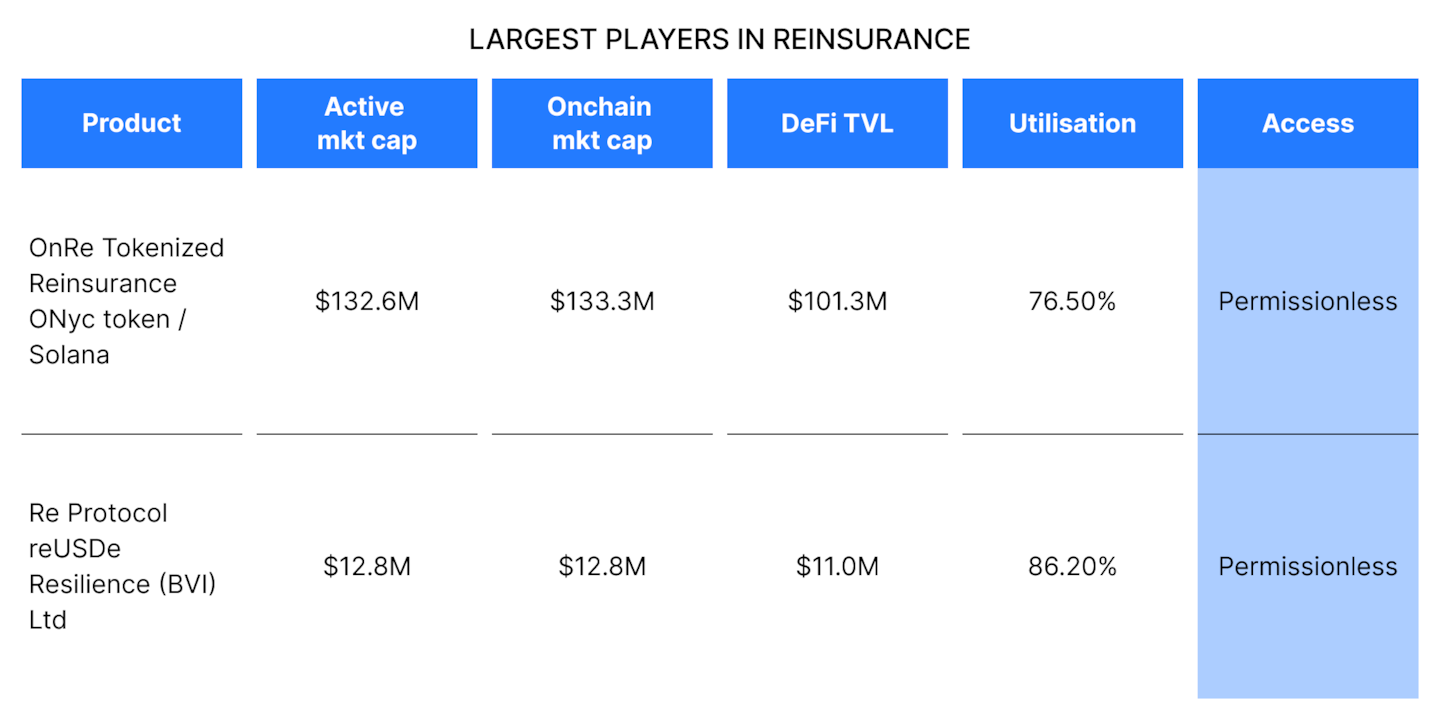

This segment is smaller in product count, but the leadership is clear. OnRe leads by both active and onchain market cap at $132.6 million and $133.3 million, with $101.3 million of DeFi TVL and 76.5% utilisation. Re Protocol reUSDe is much smaller at $12.8 million, though its 86.2% utilisation is actually higher.

The common denominator here is that both products are permissionless and tied to an asset class that has historically been hard to reach. That is likely why this category has been able to build meaningful usage despite being niche.

What has improved, and what still needs to be solved

Over the past year, several developments have pushed the tokenised private credit market forward. Three trends in particular show how the sector is evolving and becoming more integrated with both traditional finance and DeFi infrastructure.

1. Private credit funds are becoming the dominant tokenisation structure

One of the clearest shifts is that tokenised private credit is increasingly being delivered through fund structures rather than individual loans.

Earlier experiments often tried to tokenise loans directly. In practice, that proved difficult. Private loans involve complex servicing, legal enforcement, and borrower monitoring. Tokenising them one by one rarely scaled.

The market has instead moved toward tokenising access to diversified credit funds.

Apollo’s ACRED is one of the most visible examples. The product gives investors onchain exposure to Apollo’s Diversified Credit Fund, a large institutional private credit strategy. Rather than tokenising the loans themselves, the structure tokenises a feeder vehicle that allocates to the underlying fund.

2. Tokenised credit is beginning to function as collateral

Another improvement is that tokenised private credit is starting to gain real utility onchain.

For a long time, tokenised credit products mostly stopped at issuance. Investors could hold the tokens, but there was limited infrastructure around them. That is starting to change.

Apollo’s ACRED has now been integrated into Morpho, where it can be used as collateral inside lending markets. This allows investors to borrow against their private credit exposure rather than simply holding the position passively.

A similar development is taking place around Maple’s syrupUSDC and syrupUSDT tokens, which represent exposure to institutional lending strategies which also went live on Morpho and over the coming months, we can expect more of these integrations to take place across the sector.

3. U.S. regulation is starting to define the boundaries for tokenised credit

The regulatory picture in the United States has also become clearer. The SEC has not created a dedicated rulebook for tokenised private credit. But recent guidance has made it clear how these products are expected to fit within existing securities law.

In January 2026, staff from the SEC’s Divisions of Corporation Finance, Investment Management, and Trading and Markets issued a joint statement on tokenised securities. The statement emphasised that tokenisation does not change the legal nature of the underlying asset. A tokenised fund interest or credit security is still subject to the same regulatory framework that governs traditional securities.

For tokenised private credit, this reinforces the model that has already begun to dominate the market. Products like ACRED operate through regulated fund structures, feeder vehicles, and qualified investor frameworks rather than attempting to bypass securities regulation entirely.

The challenges of 2026

Despite this progress, the sector still faces several structural challenges. The following issues highlight some of the key limitations that continue to shape how tokenised private credit develops.

1. Liquidity is still limited

Tokenisation improves access, but it does not automatically create liquid markets for private credit. Most tokenised private credit products still rely on structured redemption mechanisms rather than active secondary trading. The underlying assets remain private loans, which means liquidity ultimately depends on portfolio cash flows rather than continuous market trading.

Projects are trying to address this by integrating credit tokens into lending protocols and collateral markets. The idea is that an asset does not need to trade frequently if it can still be borrowed against or used inside other financial strategies.

2. Legal structures remain complex

Another challenge is the legal architecture behind most tokenised credit products. Many tokens represent indirect claims on credit portfolios through SPVs, feeder funds, or note structures. Investors usually do not hold the underlying loans directly. Instead, they hold an interest in a vehicle that owns those assets.

This structure helps the market operate within existing regulatory frameworks. But it also introduces additional legal and operational layers between token holders and the underlying credit exposures.

So far, the market has largely accepted this trade-off. Using familiar fund and SPV structures makes it easier for institutional managers to experiment with tokenisation, even if it limits how directly assets can be represented onchain.

3. Pressure in the underlying private credit market

A third challenge comes from the condition of the private credit market itself.

In 2026, investors started to worry as cracks began to appear in the private credit market. Fitch Ratings reported that the U.S. private credit default rate rose to 5.8% in January 2026, continuing its upward climb.

The concern is also showing up in fund flows and liquidity management. Reuters reported that Blue Owl decided to sell $1.4 billion of assets, return capital to investors, and stop quarterly redemptions in one debt fund, while BlackRock limited withdrawals from a flagship debt fund and Blackstone disclosed that BCRED faced first-quarter withdrawal requests equal to 7.9% of shares.

This matters for tokenised private credit because tokenisation is often pitched as a way to open private credit to a broader investor base.

That may improve access, but it also creates a harder question. If managers expand retail distribution just as defaults rise, redemptions increase, and valuations come under pressure, new investors can start to look less like democratised access and more like a new source of liquidity for an asset class under strain.

Where could tokenised private credit go next?

Tokenised private credit is not going away. Over the past year, it has expanded from a small group of experimental structures into a broader market that now includes feeder funds, onchain lending pools, structured credit products, and reinsurance-linked strategies.

The more important question now is what the next phase of growth looks like. One obvious direction is breadth. More parts of the private credit universe could come onchain over time, including asset-backed credit, trade finance, infrastructure debt, speciality finance, and other segments where access remains limited, and ownership is difficult to transfer.

Another is participation. If early efforts continue to work, larger private credit managers may decide to tokenise more of their product shelves, not to reinvent private credit itself, but to modernise how it is distributed and accessed.

At the same time, the market’s long-term potential will depend on utility. The clearest sign of progress so far is that tokenised private credit is beginning to move beyond simple issuance and into collateral markets, lending protocols, and other DeFi use cases. If that continues, the market could evolve from a set of tokenised wrappers into a more useful financial layer within onchain portfolios.

The deeper challenge for the next phase of growth is whether the regulatory environment will allow permissionless distribution of tokenised private credit to develop alongside the permissioned track. As with tokenised stocks, regulators are broadly comfortable with tokenised credit instruments that remain within supervised custody and are distributed through controlled channels. The difficulty begins when the same instrument moves into open, permissionless DeFi, where it can be traded on decentralised exchanges, used as collateral in unregulated lending markets, or held by any wallet without KYC.

That is what to watch in 2026. Tokenised private credit has a strong path forward, but much will depend on whether the market remains largely confined to permissioned wrappers or whether regulation eventually creates room for deeper integration with DeFi.