The onchain derivatives market is currently a tale of two distinct realities. On one side, perpetual futures (perps) have found genuine product-market fit, commanding massive daily volumes that rival traditional financial systems.

On the other side, the onchain options market remains comparatively dormant. Despite clear theoretical demand for hedging instruments and volatility products, decentralised options have struggled to capture significant liquidity or volume.

The gap between these two worlds is structural rather than a lack of interest. The primary culprit is capital inefficiency. Most current decentralised exchanges (DEXs) utilise isolated margin models. In these systems, every trade operates as an island.

If a trader holds a long position and a short position that perfectly hedge each other, the protocol generally ignores the relationship. It demands full collateral for both sides, locking up capital that should be free for other opportunities.

This inefficiency renders complex strategies prohibitively expensive and keeps professional market makers firmly anchored to centralised exchanges where capital efficiency is king.

A new standard for DeFi risk

Imagine the robust risk engines of traditional finance, evolving toward a fully permissionless future. That is Kyan. It has emerged as the answer to the structural deadlock facing the current market.

Formerly known as Premia, Kyan represents a complete architectural overhaul designed to bring high-performance, portfolio-margined trading to DeFi. Currently operating as a powerful hybrid, Kyan leverages offchain matching for speed while securing deposits onchain.

This architecture is the foundation for an ambitious endgame: a trading experience that rivals the world’s largest exchanges, yet operates entirely without centralised reliance.

At its core, Kyan is best understood as TradFi-grade risk infrastructure, built natively for DeFi. Rather than retrofitting legacy DeFi primitives to handle complex derivatives, Kyan re-architects the trading stack around portfolio-level risk, capital efficiency, and professional execution standards.

The result is not just another exchange, but a foundation for sophisticated onchain derivatives markets that can support real institutional participation without compromising self-custody.

Evolving from Premia to Kyan

To understand Kyan, one must first understand its lineage. Long-time DeFi users will remember Premia as a pioneer in the options space. The protocol has iterated through multiple versions: from the peer-to-pool models of v1 and v2 to the concentrated liquidity structures of Premia Blue. Kyan is the culmination of years of live market data and user feedback.

The team realised that iterative improvements to an isolated margin model would never bridge the gap with centralised competitors like Deribit. For onchain options to succeed, the underlying financial engineering had to change. You cannot build a professional-grade derivatives exchange on infrastructure that treats every position as a separate liability. It requires a system that mathematically understands the relationship between different assets in a portfolio.

Kyan is the result of this realisation. It is a decentralised, orderbook-based exchange built from the ground up to support options, perpetual futures, and complex multi-leg strategies within a single, unified risk environment.

The core unlock: portfolio margin explained

The headline feature of Kyan is Portfolio Margin. This is the engine that separates it from the vast majority of decentralised exchanges and aligns it with traditional financial standards.

In the standard isolated-margin model found on most DEXs, risk is additive. Buying a call option requires one pile of collateral. Selling a perpetual future requires another. The system views these as two distinct dangers, even if the short future perfectly balances out the long call.

Kyan takes a holistic approach. Its risk engine evaluates the net exposure of your entire portfolio. If you hold a spot position and sell a call against it (a covered call), the engine recognises that your downside is capped. Consequently, the margin requirement drops significantly.

This dynamic approach unlocks critical capabilities:

- Greater leverage through efficiency: Your capital stretches further because the system rewards risk-reducing behaviour. A delta-neutral portfolio can access significantly higher leverage than a naked bet because the mathematical risk is lower.

- True hedging utility: A long perp can offset a short option, freeing up collateral that would otherwise be stuck. This allows market makers to quote tighter spreads since their capital costs are lower.

- Affordable complex strategies: Structures such as spreads, straddles, and butterflies become capital-efficient. Instead of paying for the max loss of every leg combined, you only pay based on the max loss of the strategy itself.

Margin requirements on Kyan update in real time as market conditions shift. The system continuously calculates the Initial Margin Ratio (IMr) to enter trades and the Maintenance Margin Ratio (MMr) to keep them open, ensuring capital efficiency never compromises the protocol’s solvency.

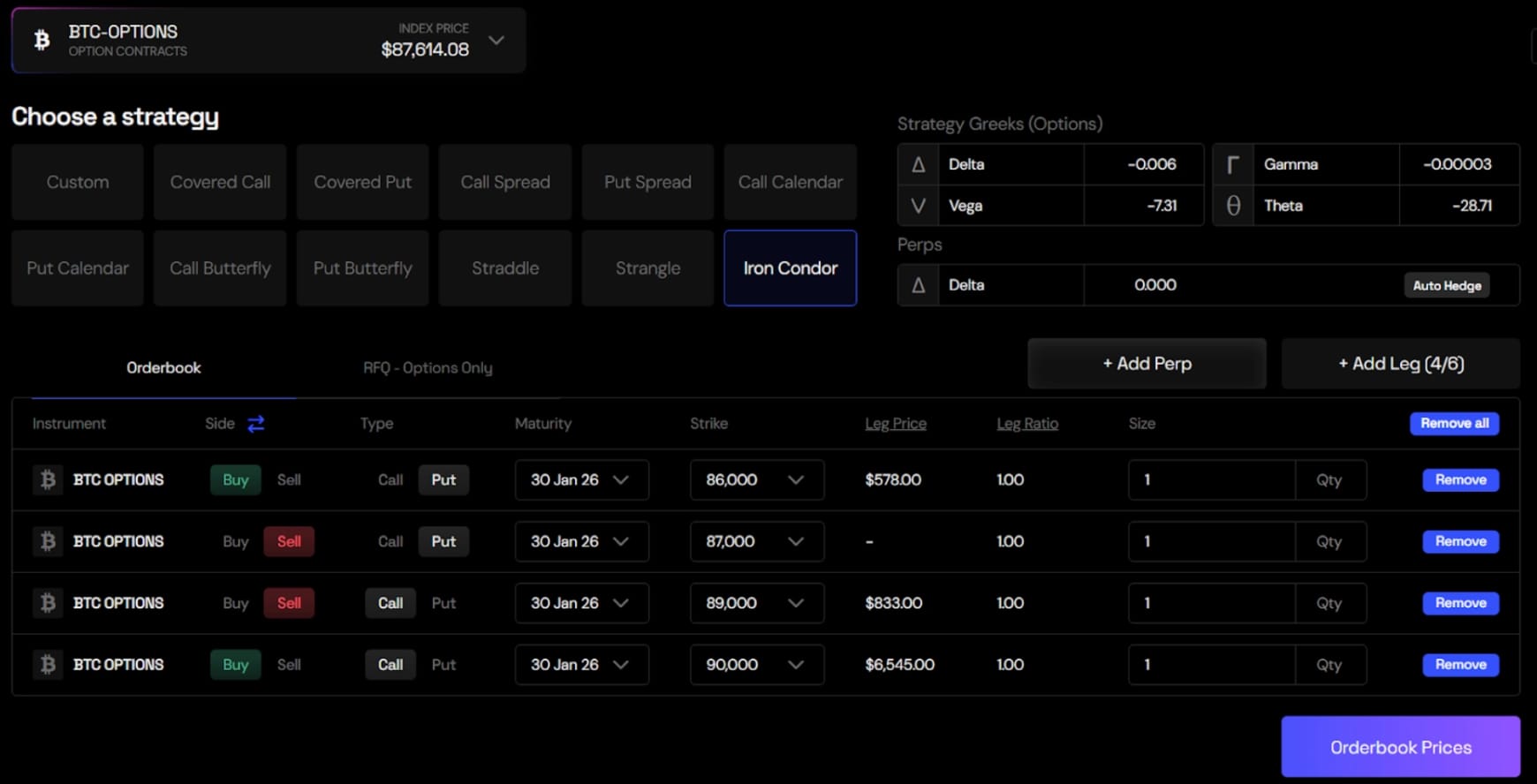

The Iron Condor problem

To visualise the power of Kyan’s portfolio margin, let’s look at a trader named Alice. She wants to execute an Iron Condor on Ethereum. This is a neutral strategy, meaning Alice is betting that the price of ETH will stay within a specific range.

An Iron Condor involves four distinct legs:

- Short Put: Selling downside risk.

- Long Put: Buying downside protection.

- Short Call: Selling upside risk.

- Long Call: Buying upside protection.

The old way (isolated margin): On a standard DEX, the protocol treats the Put side and the Call side as two separate potential disasters. It typically requires Alice to post collateral to cover the maximum possible loss for the Put side plus the maximum possible loss for the Call side.

This is capital inefficiency in its purest form. It is physically impossible for ETH to go to zero and to infinity at the same time. Alice cannot lose on both the upside and the downside simultaneously, yet the isolated-margin model bills her for both risks.

The Kyan way (portfolio margin): Kyan’s risk engine analyses the strategy as a single unit. It recognises that Alice can only lose on one side at expiration. If ETH skyrockets, the Put side expires worthless, which is a win for that side of the trade. If ETH crashes, the Call side wins.

Therefore, Kyan calculates the margin requirement based on the single largest potential loss, rather than the sum of both. This logical approach can free up to 50% of Alice’s capital compared to the isolated model. She can use that freed capital to size up her position, add new hedges, or simply keep it as a safety buffer.

Technical architecture: the hybrid model

Building a system capable of handling this level of complexity requires robust infrastructure. Kyan utilises a hybrid approach that combines the performance of off-chain matching with the security of on-chain settlement.

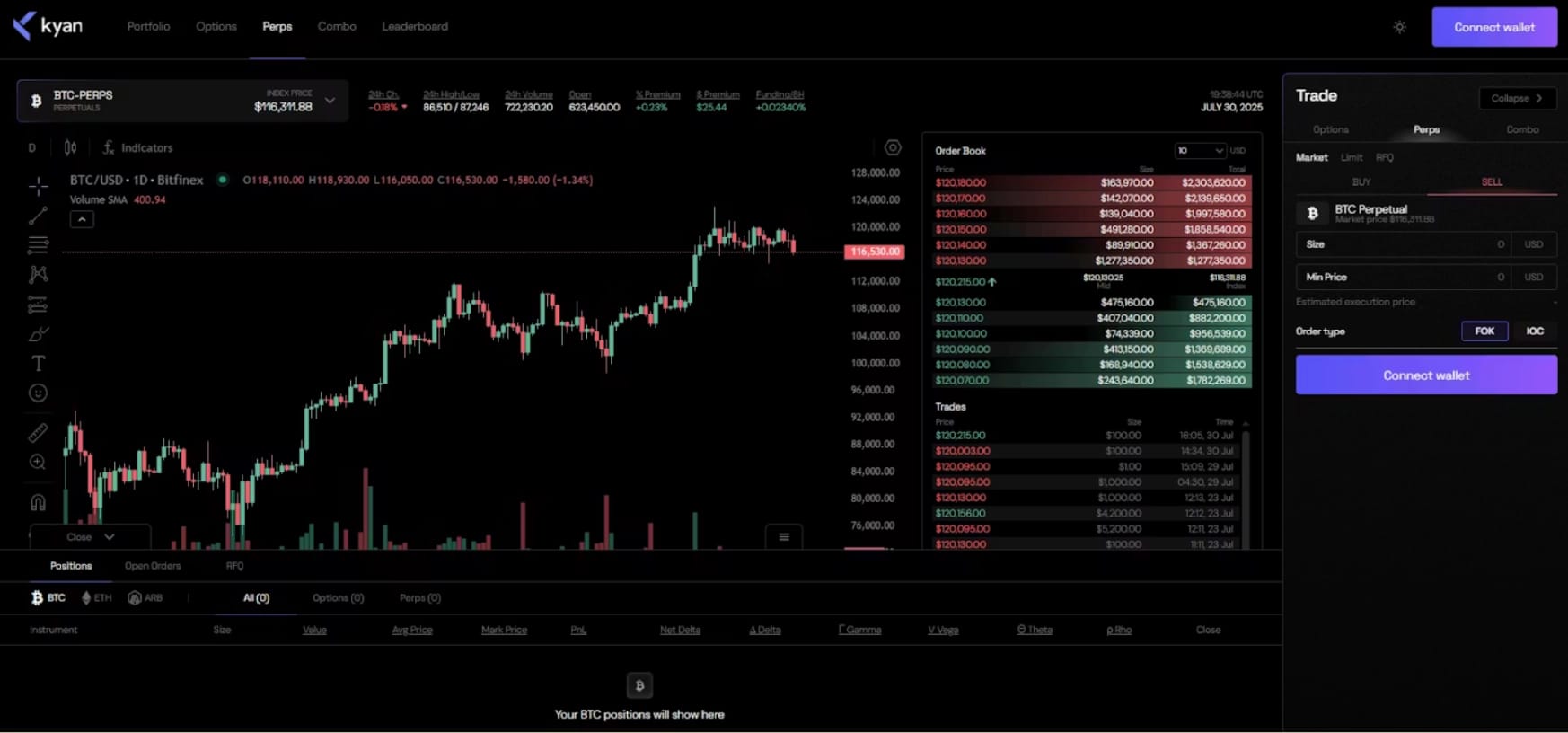

The Central Limit Orderbook (CLOB)

Automated Market Makers (AMMs) changed the game for simple token swaps, but they often fail when applied to options. Options are complex instruments with time decay and constantly shifting volatility. In a passive AMM pool, liquidity providers often cannot update their pricing fast enough, leading to losses against sharp traders.

Kyan replaces the passive AMM with a Central Limit Orderbook. This structure allows professional market makers to provide active liquidity. They can update their quotes thousands of times per day based on real-time data without paying gas fees for every change. For the user, this results in tighter spreads, deeper liquidity, and fair pricing that reflects the true state of the market.

Atomic execution and “legging out”

One of the most significant pain points in DeFi options is execution risk on multi-leg strategies. If a trader wants to execute an Iron Condor on a typical AMM, they often have to execute each leg individually.

This creates a dangerous phenomenon known as “legging out.” Imagine Alice buys her protective legs, but before she can sell her short legs, the market moves violently. She is now stuck in a partial position that does not align with her strategy, exposing her to risks she never intended to take.

Kyan solves this with atomic Combo Trades. Users can construct strategies with up to seven different legs and execute them as a single order. These are processed as Fill-or-Kill (FOK) orders. This means the engine guarantees that either the entire strategy executes at the desired price, or none of it does. There is zero risk of partial fills.

Smart Accounts and gasless trading

High-frequency trading is impossible if you have to pay gas fees for every order modification. Kyan utilises smart account infrastructure (leveraging account abstraction concepts) to offer a gas-free trading experience.

Users sign intent-based messages to place and cancel orders. These actions are cryptographically secure but do not require an on-chain transaction until settlement occurs. This removes the friction of approving every single action in a wallet popup, bringing the user experience in line with the smooth interface of centralised exchanges.

A unified trading experience

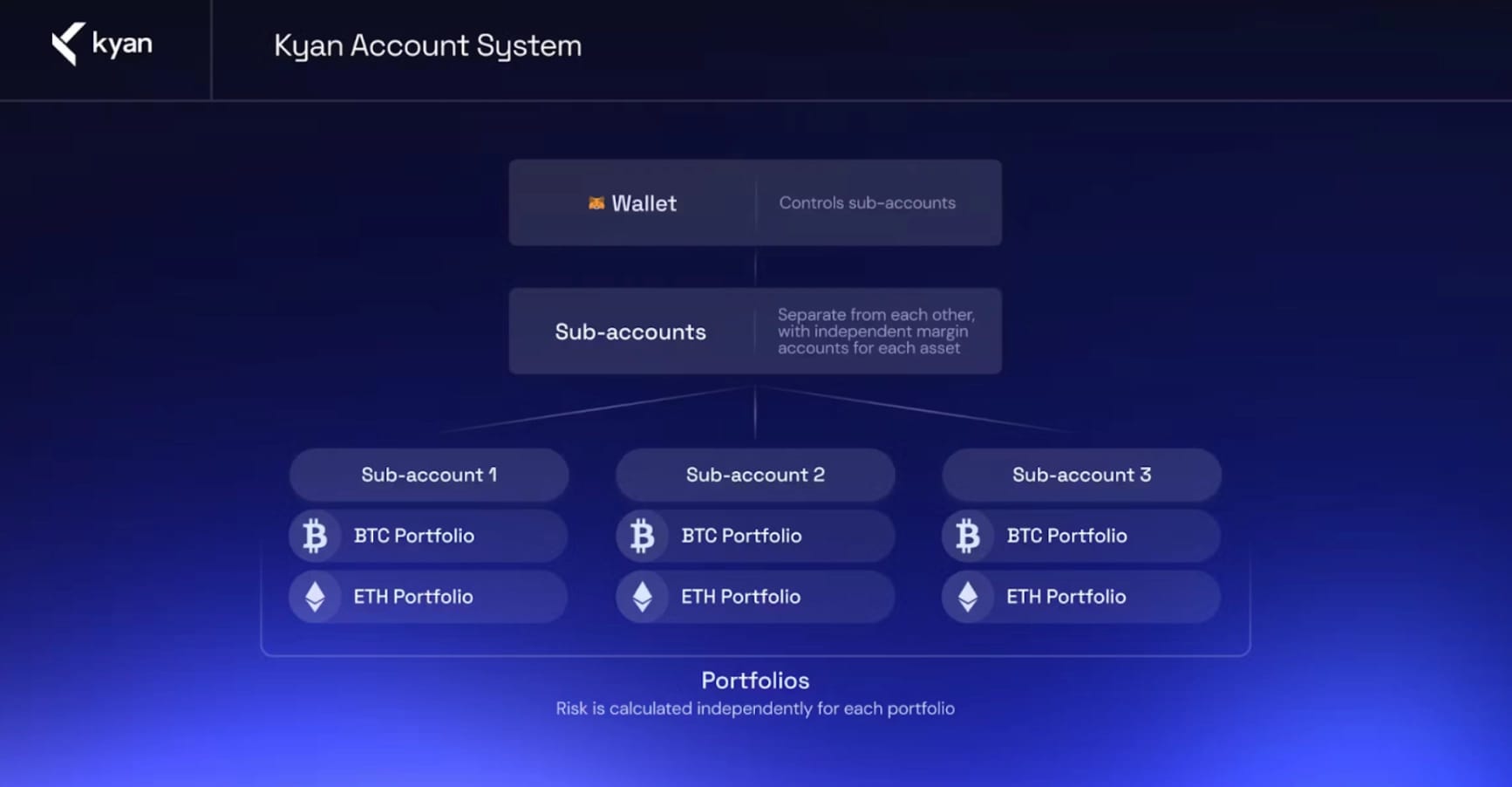

Kyan moves away from the fragmented liquidity models of the past. The CLOB houses both options and perpetual futures for each specific asset. This consolidation is critical because it enables cross-instrument hedging.

Because Kyan segregates risk by asset (e.g. BTC and ETH portfolios are distinct), this structure allows you to offset your options exposure with perpetual futures on the same asset. You can manage your entire position, including puts, calls, and perps, within a single, unified interface.

The trading experience is designed to feel familiar to institutional traders while retaining the benefits of DeFi self-custody:

- Request for Quote (RFQ): For large block trades that might suffer from slippage on the public orderbook, Kyan supports RFQ orders. This allows traders to request custom pricing directly from market makers for specific sizes or complex structures, ensuring execution quality for institutional-sized flows.

- Single interface for all greeks: Managing a complex portfolio often involves toggling between five different tabs to check delta, gamma, and vega exposure. Kyan unifies everything. A trader can view their aggregate exposure across all options and perps in a single dashboard, allowing for instant risk assessment.

Safety first! Risk management and liquidation

With the introduction of portfolio margin and higher leverage comes the need for robust risk management. Kyan evaluates account health using two primary metrics that update with every tick of the market:

- Initial Margin Ratio (IMr): This is the capital required to enter a new trade. It acts as the first line of defence, ensuring traders are well-capitalised before taking on exposure.

- Maintenance Margin Ratio (MMr): This is the absolute minimum capital required to keep the trade open.

If an account falls below the maintenance threshold, the liquidation engine activates. However, Kyan avoids the “instant death” liquidation model seen on some high-leverage platforms where the entire account is market-sold instantly.

Instead, it employs a gradual liquidation process. The system prioritises risk reduction. It algorithmically selects the specific positions to close that will reduce the portfolio’s risk exposure the most while incurring the lowest cost. It closes only enough volume to bring the account back to health. This protects the user from total loss during momentary wicks and protects the orderbook from absorbing massive liquidation cascades.

Who is Kyan for?

Kyan is positioning itself as a critical infrastructure for sophisticated market participants.

- Funds and trading desks: These users require portfolio margin to run their strategies effectively. They cannot afford to lock up 100% collateral for hedged positions. Kyan offers the capital efficiency they are used to in TradFi, but onchain.

- Advanced retail: Traders who have “graduated” from simple directional perps and want to express views on volatility, time decay, or specific price ranges will find Kyan’s tooling unmatched.

- Structurers: The ability to execute atomic multi-leg strategies makes Kyan a prime venue for building structured products. Developers can build “vaults” or “yield products” on top of Kyan that execute complex strategies with a single click.

Road to Mainnet

The journey to launch has been rigorous. The Testnet Alpha phase concluded in December, rewarding the top traders with Krystals and USDC for stress-testing the portfolio margin engine under real market conditions.

For those who missed the first round, a final opportunity is approaching. Kyan will host a Public Beta from February 2nd to February 8th. This limited-time event allows users to earn Krystals by trading on the testnet environment before the platform goes live.

Following the Public Beta, Kyan projects a limited-access mainnet launch. Priority access will be granted to early community members and partners, making participation in the upcoming beta a strategic move for those looking to secure their spot in the initial cohort.

For traders tired of choosing between the performance of a centralised exchange and the custody model of a decentralised one, Kyan offers a compelling third path: professional-grade derivatives trading, finally brought to DeFi without compromise. It does not simplify the problem but rather engineers it properly.

Learn more or participate via: