It feels as if institutions, treasuries, and long-term investors have increasingly announced they hold Bitcoin as part of their operations. As their ownership behaviour shifts, it is likely that market expectations of the asset shift with it. Traditional assets often have a yield-bearing component. This is a result of capital markets built around such assets. You can use it as collateral to loan against or underwrite derivatives against. The reason a bank makes money is that you deposit assets within their custody, which enables them to make loans against as collateral. In comparison to these traditional yield-bearing assets, holding BTC without a generating yield component essentially leads to a yield opportunity cost. For too long, that gap has persisted.

That forthcoming opportunity set for yield is the idea behind BTCFi. Let’s take a closer look.

Within this article, we will define BTCFi for broader audiences, examine an expected demand surge throughout 2026, and assess how the Layer 2 Starknet is well-positioned to capture that shift. As the zk L2 first mover with a well-renowned cryptography team base, can Starknet fill this long-empty vacuum and become the de facto execution hub for BTCFi activity?

Why should I care about the BTCFi opportunity??

BTCFi 101 and the why behind the excitement

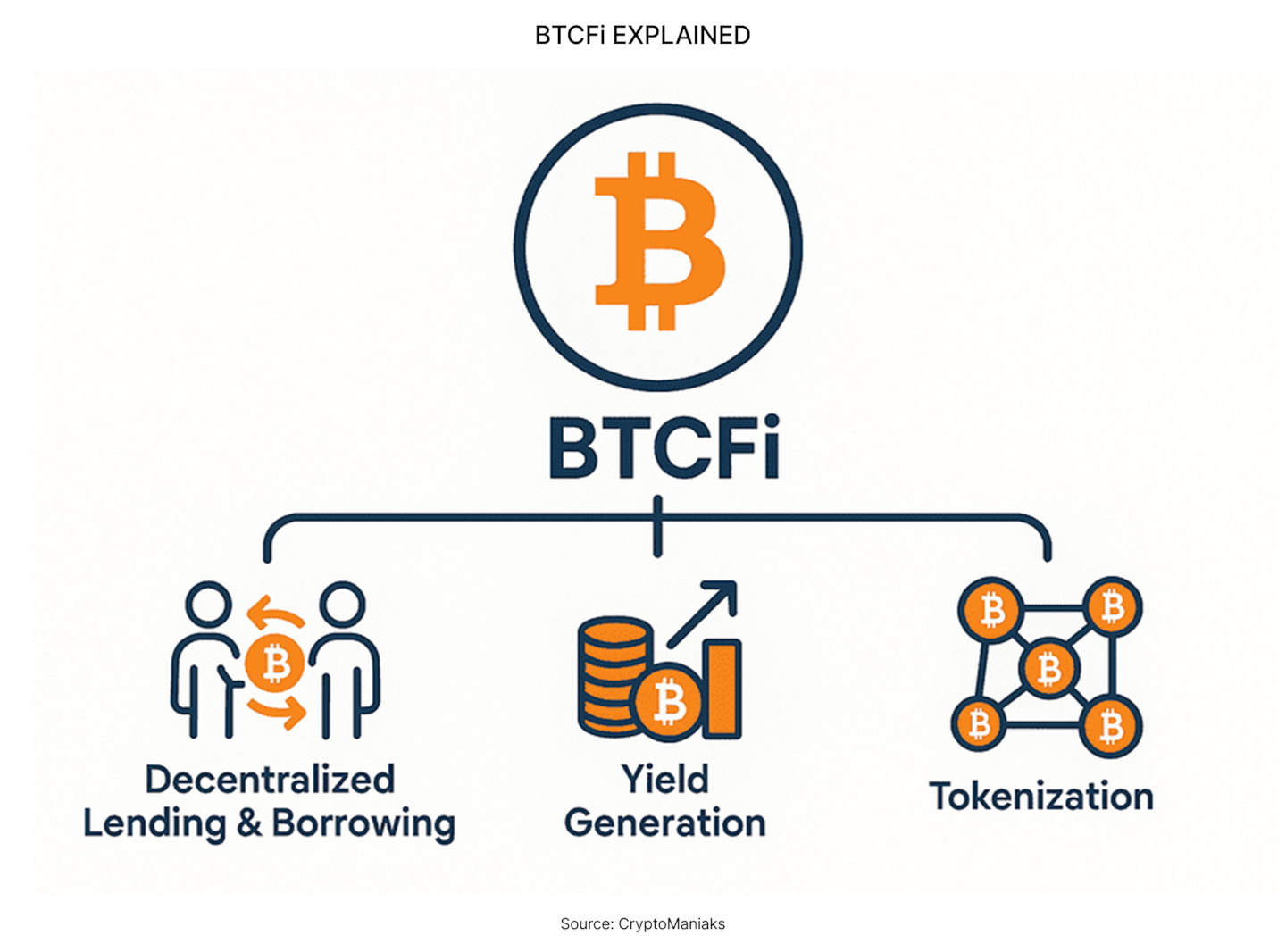

BTCFi can be best understood as the effort to transform Bitcoin into a “productive” asset without requiring holders to sell their BTC.

This is enabled in several ways (which are not limited to): lending out BTC to generate yield, borrowing against BTC to access liquidity without exiting exposure, deploying BTC liquidity to earn trading fees, or running structured strategies that generate carry while remaining long BTC. Sound complicated? These are things that are readily available for stocks and hard assets like precious metals or real estate.

Historically, BTC holders have HODLed. As a result, they have not focused much on generating yield from their BTC holdings. But now, excitedly, as BTC has entered a phase of institutionalisation and is starting to appear on balance sheets and within ETFs, the landscape is changing. We see it in the daily news items.

For capital allocators operating under mandates and benchmarks, BTC is assessed alongside other asset classes. Without a yield component, it can appear inefficient compared to alternatives, encouraging the search for yield to deliver higher returns.

Institutional Bitcoin is coming into play. What size do you ask?

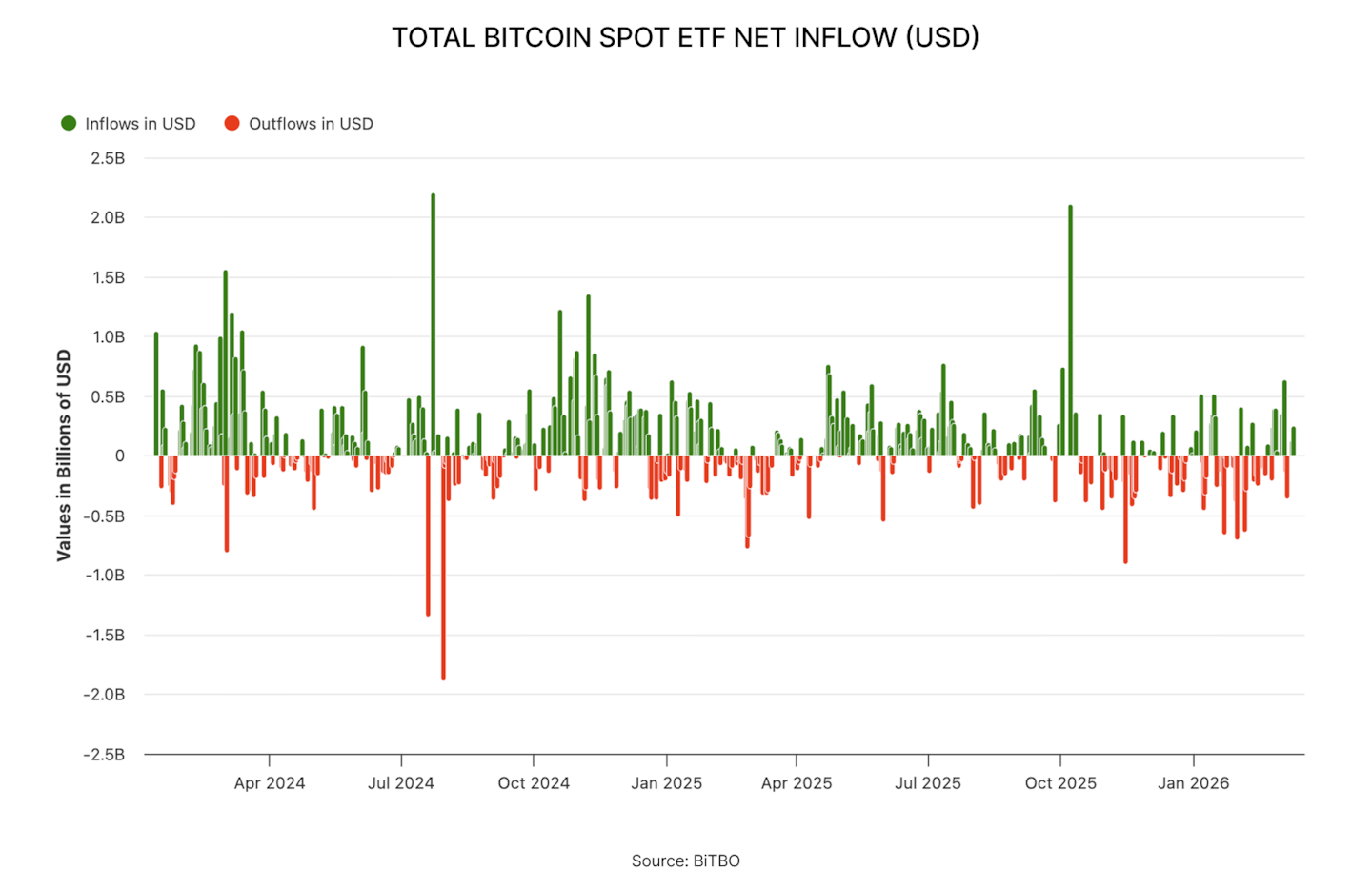

Between 2024 and 2025, Bitcoin has moved closer to the long-awaited mainstream adoption. The approval of U.S. spot Bitcoin ETFs in January 2024 opened a direct path for traditional investors. This led to quick and steady inflows. As of now, ETFs hold $100 billion in BTC, representing 7% of the total circulating supply.

Corporate balance sheets have also seen the addition of BTC rise sharply. As of February 2026, public companies hold $73.80 billion in BTC, representing 5% of the total supply. Adding to the mix, Private companies hold $29.32 billion, making up another 2% of the total supply.

Taken together, BTC held in ETFs and corporate treasuries already accounts for a combined 14% of the total supply. While ETFs naturally move more slowly given the governance and operational requirements of their mandates and more conservative approach, they represent a sizable opportunity. With stablecoins, we’ve seen a similar moment where users realised they could also earn yield on the underlying collateral held for the stablecoin issuers. For example, Circle’s revenue sources are the yields on the short-term treasuries they earn on USD fiat stable deposits from approved minters. New stablecoins have increasingly shared that yield with their users.

Bitcoin is primed for a similar shift. Hard assets are proven to safely generate yield, so it’s only a matter of time. The Bitcoin held by public and private companies alone already represents a substantial untapped pool of BTC that could potentially participate in BTCFi.

Wen? 2026: the Primed Turning Point for BTCFi

The question is whether 2026 could be the year when BTCFi finally sees meaningful adoption. We argue that for this to happen, three conditions must be met.

- Institutional investors hold a large share of BTC. For BTCFi to matter in 2026, we need BTC held by allocators who account for opportunity cost and seek ways to generate yield. This includes ETFs, corporate treasuries, hedge funds, and family offices.

- Institutional deployment pathways are solid. Aside from simply holding BTC, there must also be clear regulations, custody frameworks, accounting rules, and security standards in place for institutional investors to feel comfortable deploying their BTC into BTCFi.

- If interest rates are cut, BTC can benefit as investors move further into risk assets. Lower rates increase liquidity and reduce returns on safer assets like U.S. Treasuries

Arguably, given the large size of institutional BTC already at play (14% of total supply), the first of these three conditions has already been met heading into 2026.

Another potential tailwind could come from sovereign adoption. At the time of writing, $36.89B of BTC (2.469% of total supply) is held by countries, mostly through seizures or strategic holdings. But if inflation remains persistent and currencies continue to be debased, governments may start looking for additional reserve assets.

Historically, countries have turned to hard assets like gold to protect reserves during periods of monetary instability. Bitcoin could begin to play a similar role, particularly for countries that want to diversify away from large holdings of foreign currencies or U.S. Treasuries.

What will also be important for both institutions and nation-states is having a way to maintain privacy in a compliant manner when acquiring BTC or interacting with DeFi. This is important not only for regulatory compliance but also to avoid announcing purchases to the world and losing a competitive advantage. The availability of such infrastructure would help onboard institutions and sovereign actors to BTCFi.

The remaining questions are whether regulatory progress and institutional infrastructure will catch up, and whether the macro environment continues to highlight the opportunity cost of non-yielding BTC. Those factors will determine whether 2026 becomes a turning point for BTCFi or whether adoption develops more gradually.

Starknet’s bold bet on becoming the BTCFi hub

If 2026 proves to be the year BTCFi sees meaningful adoption, the next logical question is where that BTC will be deployed and which ecosystem is best positioned to capture that activity.

Starknet is one of the largest and proven networks with a meaningful stake in this race. Through a series of infrastructure improvements and the launch of an incentive program, it is making a serious bid to position itself as the leading BTCFi hub.

Investigating Starknet’s architecture

For large-scale deployment of BTC in DeFi, the base-layer architecture must meet security requirements and minimise operational friction to satisfy the needs of professional investors.

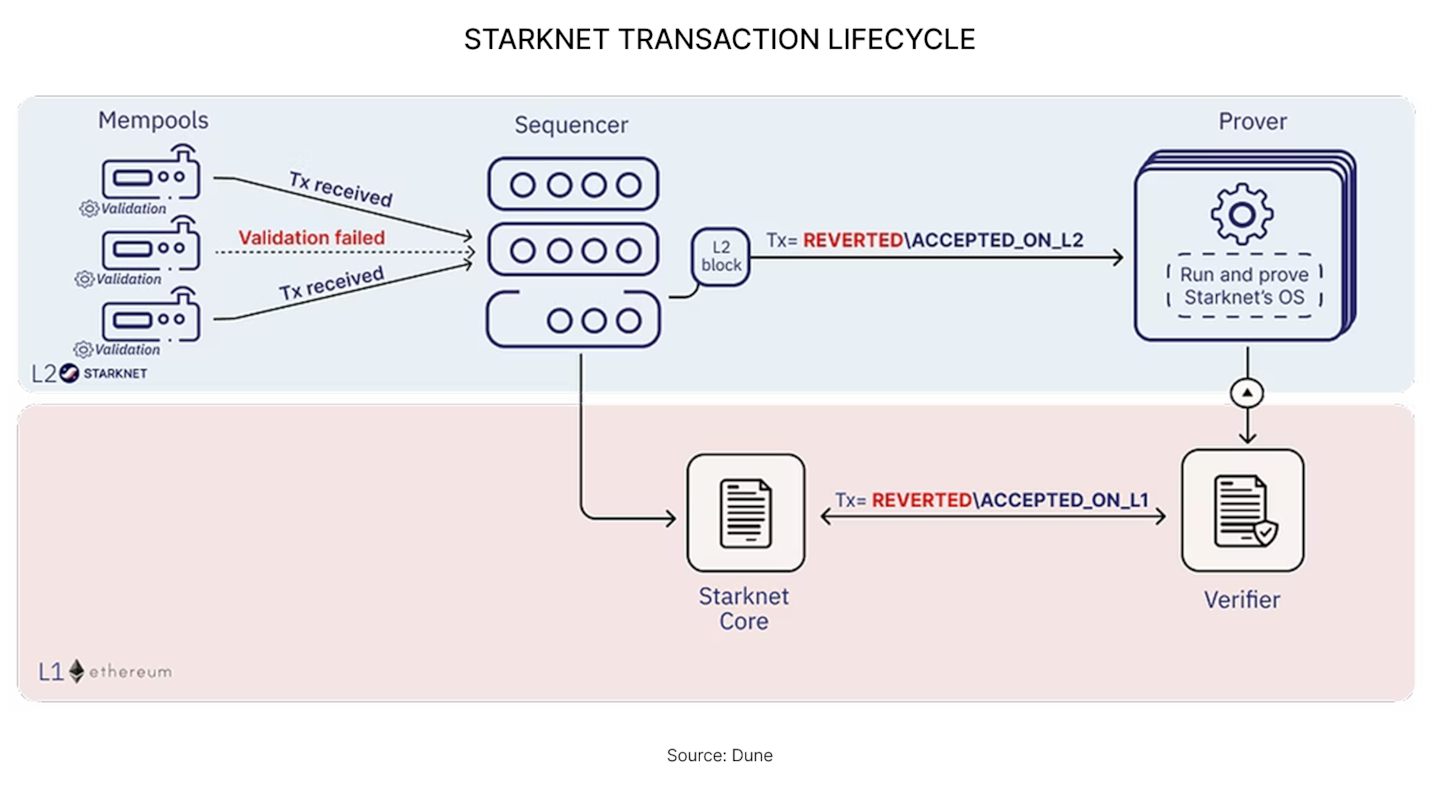

Over the years, Starknet has been steadily working toward that goal. On Starknet, transactions are executed off-chain, but their correctness is cryptographically proven and verified on Ethereum, so users do not have to trust Starknet itself to accept the outcome.

This design has enabled Starknet to be sufficiently performant to handle use cases that require high Transactions Per Second (TPS) and involve multiple steps, as many more complicated BTCFi strategies may require.

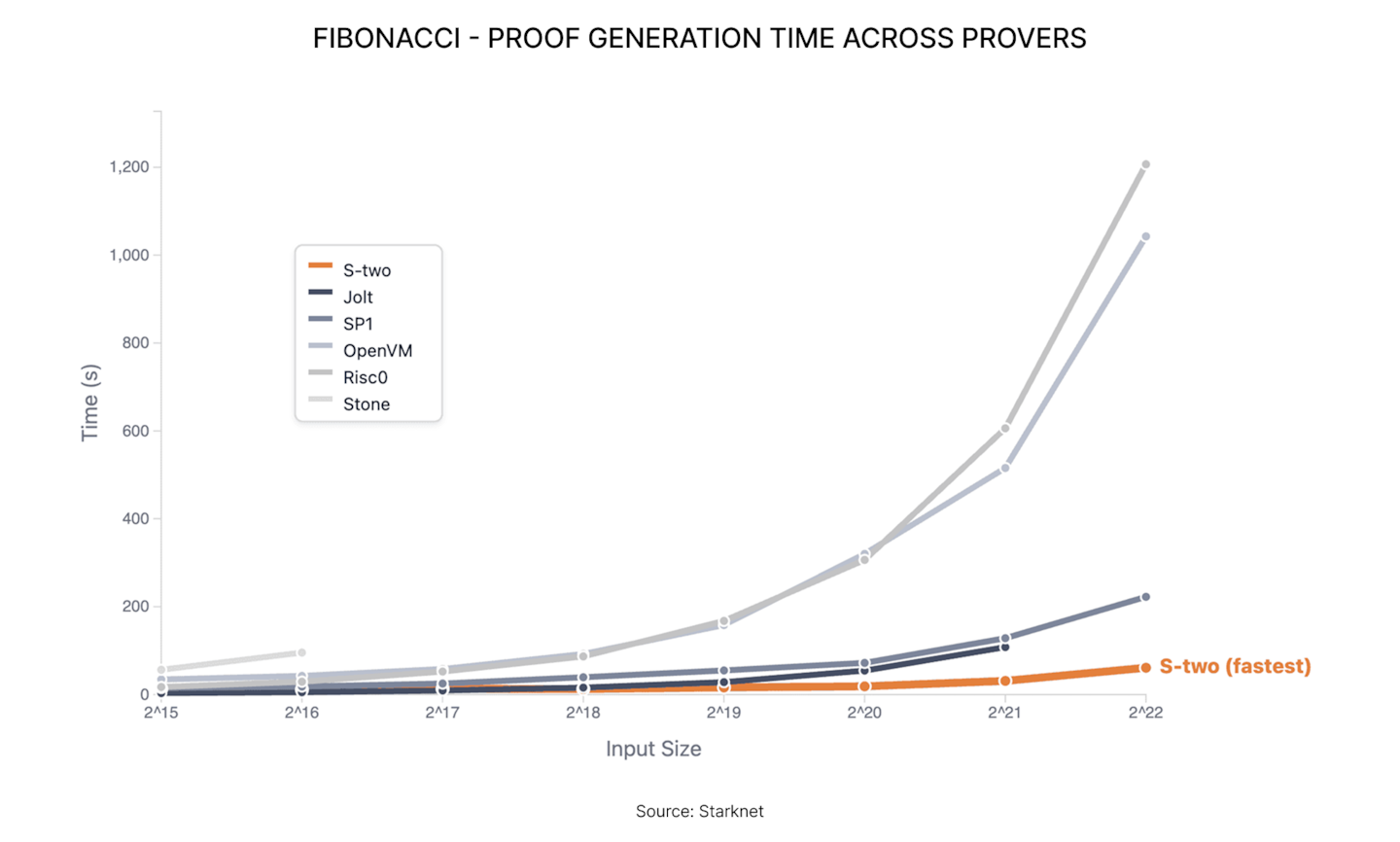

One of the most recent steps Starknet took to improve its performance was upgrading its prover, switching from Stone to S-two. The main benefit of this upgrade was that Starknet has greatly reduced proof generation time and costs. Benchmarks show that generating proofs now takes seconds instead of minutes. In a world where Vitalik has explained EVM blockchains moving towards ZK / alternate VMs and a need to be quantum proof, performance is another way of framing future-proof.

With S-two now live, Starknet’s overall costs should decrease as proof generation becomes more efficient. It also opens up new use cases. Developers can now build privacy layers, identity systems, and other applications that were once impractical due to performance or cost issues.

This technical stack has been developed over several years and is tightly integrated with Starknet’s Cairo VM and ZK proving system. For competitors to catch up from a technical perspective, they would likely need to rebuild large parts of their execution and proving infrastructure, creating a meaningful barrier to entry.

The Chain with BTCFi Season

Beyond improvements to its technical architecture, Starknet has also taken a more decisive step toward positioning itself as a BTCFi hub with the launch of BTCFi Season in October 2025, an incentive program designed to attract BTC into the ecosystem.

The program launched with an initial budget of 100M STRK, allocated to protocols that enable highly liquid BTC pools on DEXs and money markets, as well as to stablecoin borrowing against BTC collateral.

While Starknet has previously launched incentive programs, such as its DeFi Spring program in 2024 (90M STRK), this is the largest incentive program on the chain to date, underscoring the size of the bet for Starknet.

Bitcoin staking as part of existing network inflation

However, the biggest commitment of Starknet to its BTCFi strategy is that the network enables BTC holders to stake their BTC. By allowing Bitcoin staking, Starknet makes BTC a part of its security model.

Currently, staked Bitcoin can make up 25% of the network’s consensus power, while STRK holds the majority. This keeps STRK central to Starknet’s security, while BTC holders can play an important role in protecting the network.

The idea behind this move is that BTC is already a well-established asset in the crypto space. As a result, Bitcoin holders require lower rewards than holders of other tokens to participate in similar programs, making it cheaper for Starknet to secure the network.

It also offers a lower-risk way for users to earn yield by staking their BTC on Starknet. This is simpler than other DeFi strategies, like lending or providing liquidity. It provides an easy entry point into the Starknet ecosystem for BTC liquidity.

Ecosystem Readiness and Distribution

While a solid technical architecture for the chain is one thing, onboarding institutional investors into the ecosystem also requires the right infrastructure to participate in DeFi, as well as an ecosystem of assets and applications they can trust.

Starknet has taken several concrete steps to move into that position.

Custody, Onboarding, and Institutional Access

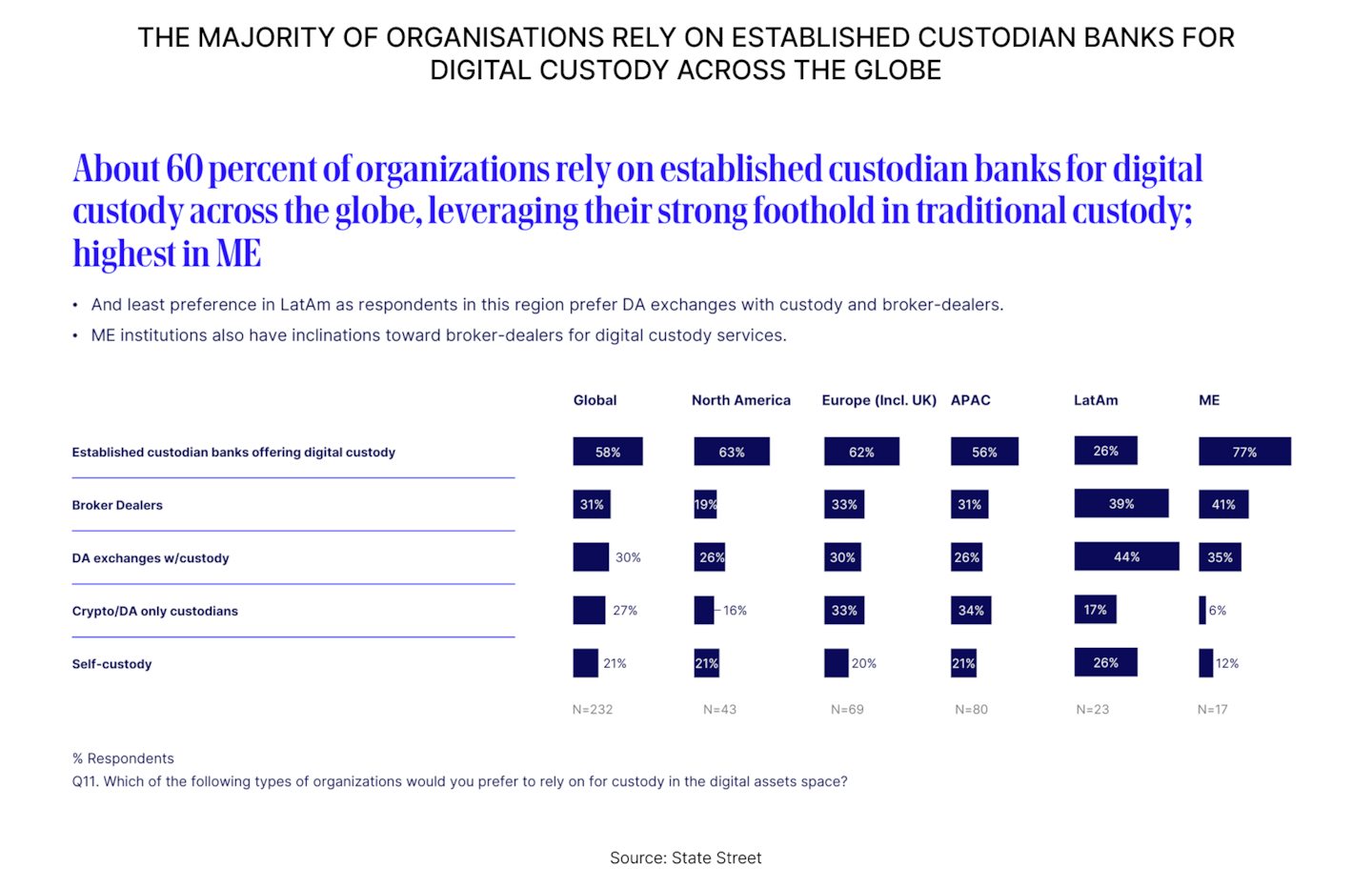

For BTCFi to see more institutional adoption, chains need custody infrastructure and tools that meet current standards. Custody rules, operational controls, and strict risk requirements constrain asset managers. If using BTC in DeFi means leaving that regulated environment, it is a no-go for them.

A 2025 global survey by State Street of 232 institutional organisations supports this view. It found that 58% of respondents rely on established custodian banks for digital asset custody, rather than crypto-native custodians or self-custody. Custodians are the gateway to onboarding institutions.

Starknet is making progress in this area. Regulated custodians like Anchorage Digital support Bitcoin staking on StarkNet. This allows institutional clients to earn staking rewards while remaining in a regulated custody environment. It tackles a key issue for institutions that cannot self-custody or engage directly with DeFi protocols.

Starknet’s native account abstraction enhances this advantage. Features like spending limits, custom authentication, recovery logic, and gas abstraction give institutions, treasuries, and DAOs the tools they need to manage risk.

At the asset layer, Starknet supports various BTC representations, including WBTC, tBTC, LBTC, SolvBTC, and liquid-staked variants. This provides onboarding flexibility and allows institutions to choose which type of BTC representation they want to have exposure to. However, it also leads to liquidity fragmentation, as more liquidity is required to increase pool depth across these different assets.

Starknet has also introduced strkBTC, a Bitcoin wrapper designed to enable private balances and transactions through Starknet’s zero-knowledge infrastructure. We will explore Starknet’s privacy architecture in more detail in the next article.

Benchmarking Starknet’s BTCFi Yields Against the Market

This section compares BTCFi yields on Starknet with those of other ecosystems in four areas: BTC staking, money markets, liquidity provision, and structured products.

How much of Starknet’s yield comes from sustainable factors versus incentives? This will help us determine whether yields are driven by long-term economics or short-term incentives, and provide a full picture of where Starknet currently stands.

1 | BTC Staking

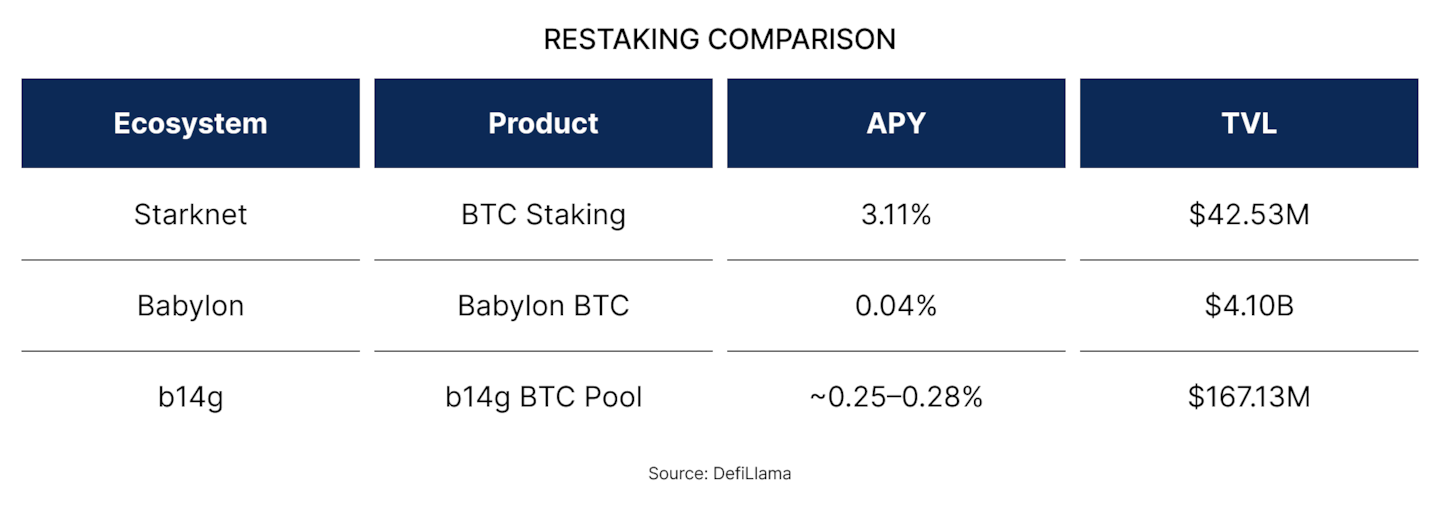

Starknet currently offers materially higher BTC staking yields than larger alternatives, but at a much smaller scale. Babylon is currently the largest Bitcoin restaking protocol, while b14g is a modular dual-staking layer for Bitcoin that ranks second in BTC restaking TVL.

The comparison focuses on Babylon, b14g, and Starknet because Babylon and b14g are currently the two largest BTC restaking protocols by TVL.

The yield difference mainly depends on scale. Starknet, with $42.53M in BTC staked, offers higher APYs than Babylon ($4.1B TVL) or b14g ($167.3M TVL). Lower APYs can partly be explained by the fact that these protocols share rewards with a much larger pool of liquidity. They also allocate fewer emissions to their security budgets.

Starknet’s staking TVL stands at $97.89M, with about 57% in STRK ($55.36M) and 43% in BTC ($42.53M). For a new mechanism, BTC participation is meaningful, but it remains early stage compared to larger staking ecosystems.

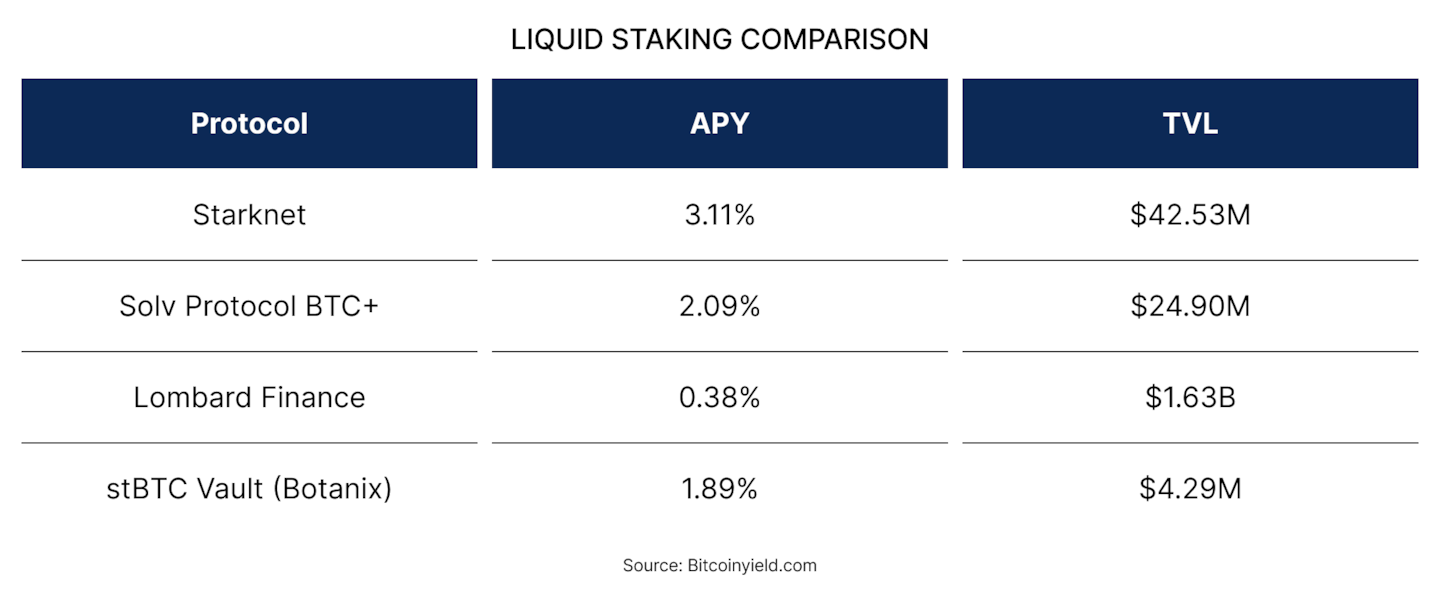

Beyond traditional restaking protocols, Starknet also compares favourably with liquid staking and restaking protocols such as Lombard Finance, SolvBTC, and stBTC. Staking on Starknet can offer a higher APY than simply holding these protocols’ liquid staking tokens.

Importantly, BTC staking rewards are not tied to short-term incentives. Under the protocol design, BTC stakers earn 20–25% of the total STRK rewards minted. This embeds BTC rewards directly into the staking framework, making them structurally supported rather than dependent on temporary programs.

However, current yields do reflect a competitive launch phase. As BTC staking increases, staking APY will likely decline as rewards are distributed across a larger pool of participants.

2 | Money markets

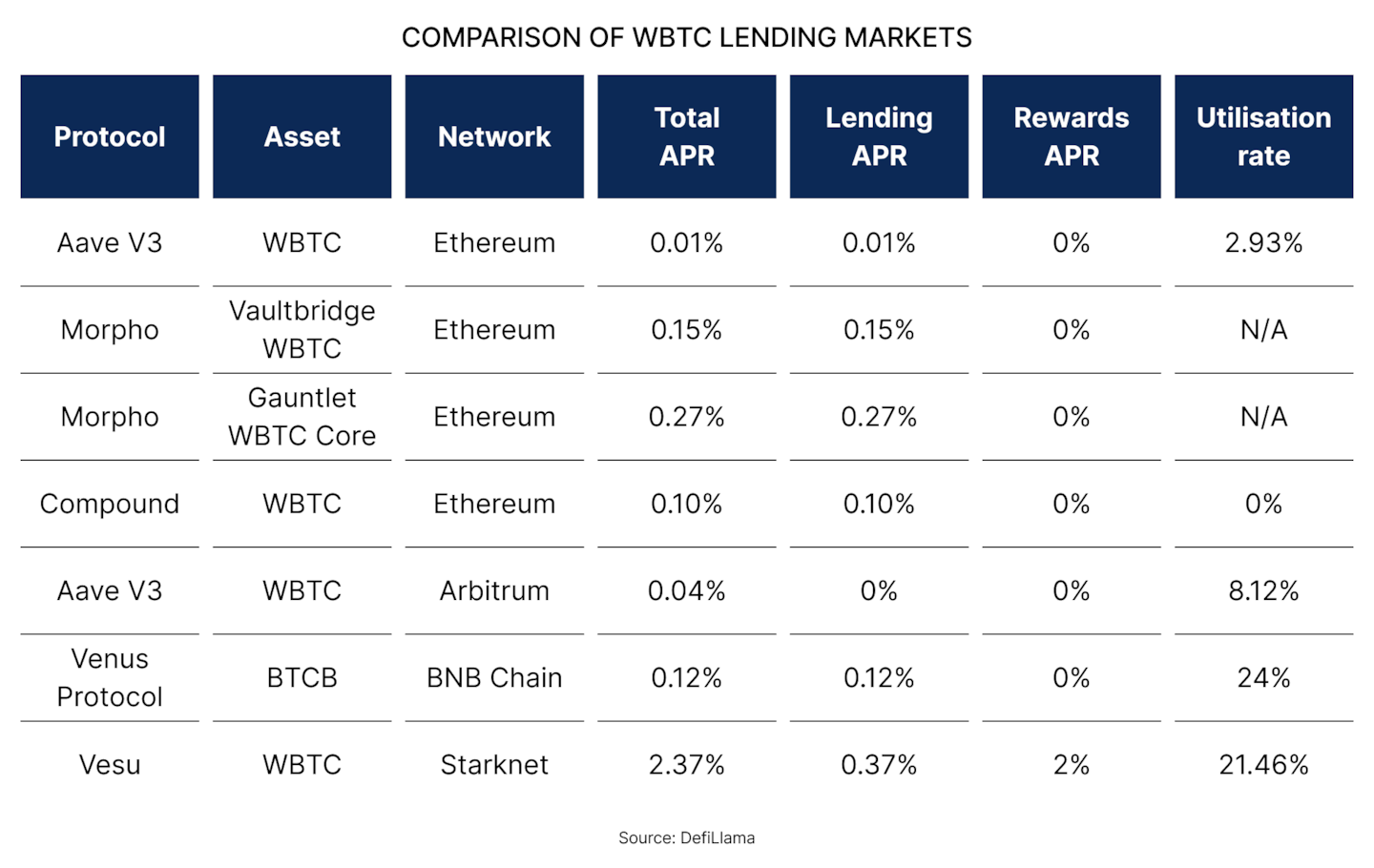

Vesu is the largest lending protocol on Starknet, with a total TVL of $26M. This comparison looks at Vesu’s WBTC market and its supply-side APRs, alongside major WBTC markets from other lending platforms.

On Ethereum, Arbitrum, and BNB Chain, the APR on WBTC lending ranges from 0.01% to 0.27%. All of the lending markets offer no additional supply-side incentives, and utilisation rates are low, ranging from 2.93% to 24%.

In contrast, Vesu’s WBTC market on Starknet shows an APR of 2.37%. The headline APR comprises a 0.37% lending APR, a 2% rewards component, and a utilisation rate of 21.46%.

The yield difference mainly comes from incentives. The 2% rewards significantly raise the headline APR, suggesting a bootstrapping phase rather than a stable market price.

Despite this, Vesu’s base lending APR is 0.37%, higher than in any other lending market we analysed. Utilisation is also higher. At 21.46%, it is more than seven times the utilisation of Aave V3 on Ethereum (2.93%) and sits toward the upper end of comparable markets. This points to strong demand for WBTC borrowing on Starknet.

In addition to wBTC, there are other BTC wrapper opportunities which are not highlighted here, such as tBTC, lBTC, and solvBTC.

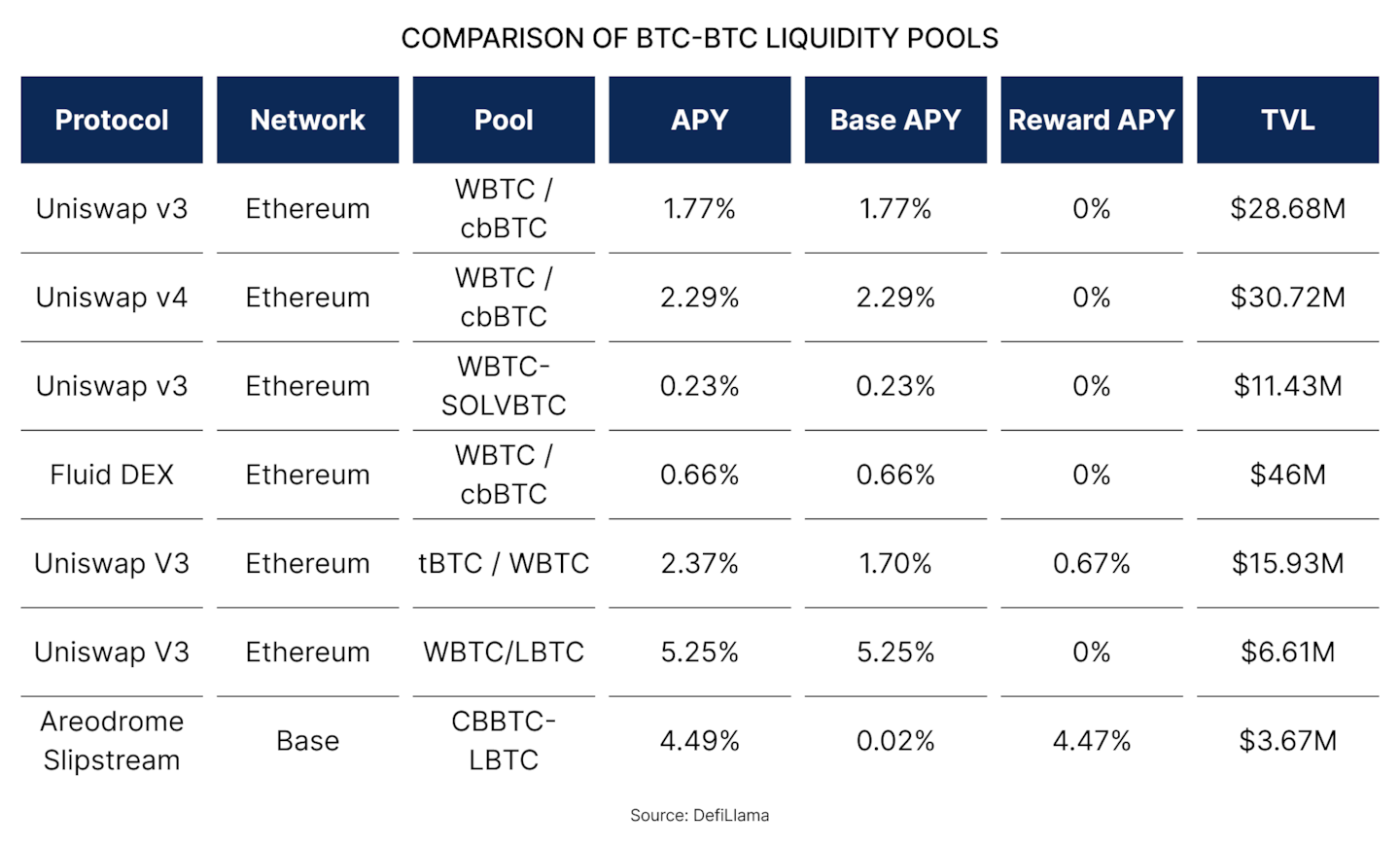

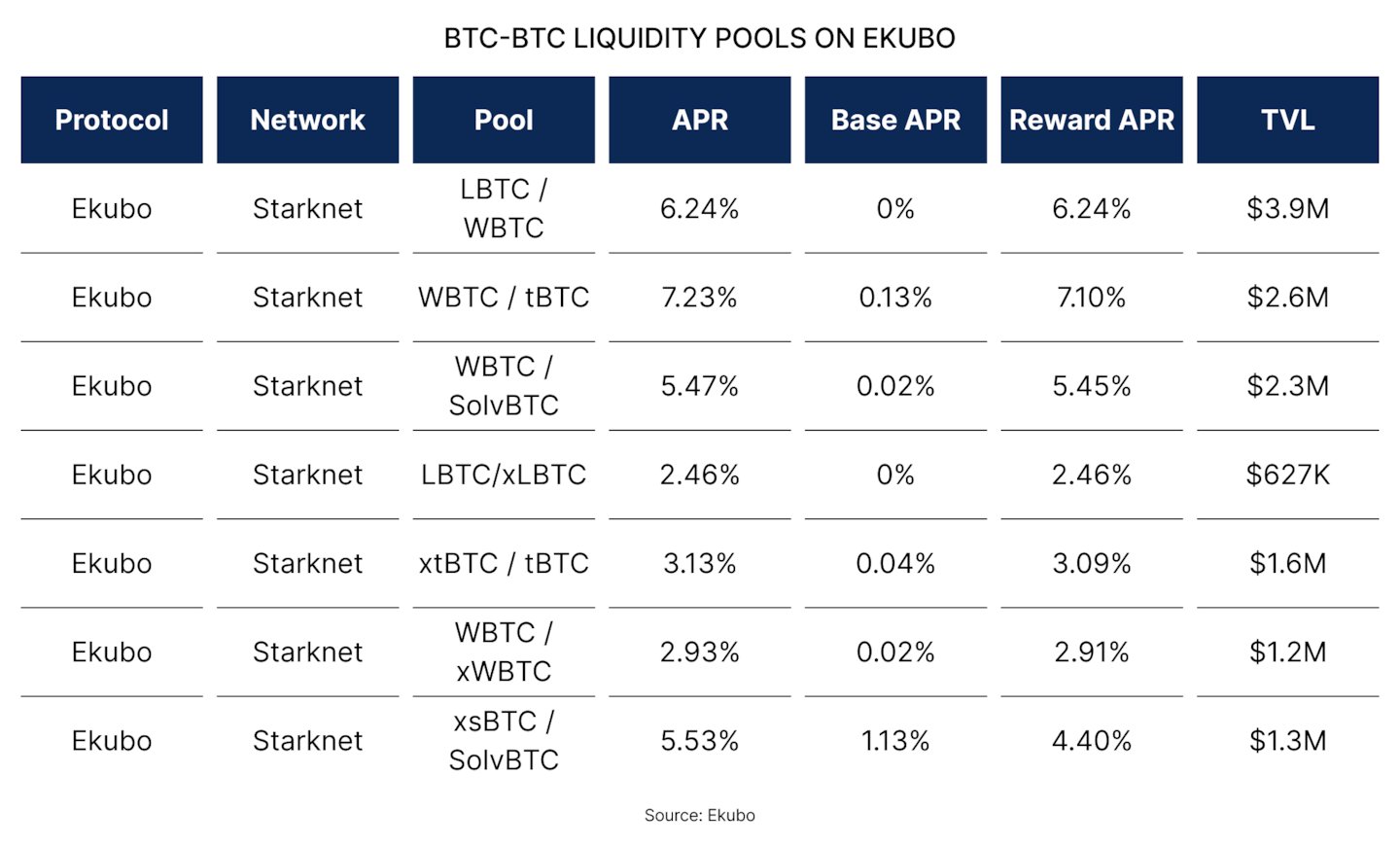

3 | LP Positions

Ekubo is the largest DEX on Starknet, boasting $35M in TVL. Here, we compare BTC–BTC liquidity pools on Ekubo with popular ones on other platforms. We focus on pools that allow liquidity provision without exposure to non-BTC assets.

On established DEXs like Ethereum, wrapped BTC–BTC pools mostly offer lower, fee-based yields.

Most APY in these pools comes from trading activity (vs incentives). The base APY ranges from 2.29% to 0.02%. The main exception is Aerodrome Slipstream, which gets most of its 4.49% from incentives.

Currently, the pool with the highest APR is xsBTC/SolvBTC at 7.23% and ranges between 3-7% in comparison with 0-5% captured on Ethereum.

Ekubo provides competitive headline yields for BTC–BTC pools. However, these APYs are primarily driven by incentives, while the fee-based base APR is lower than that of most established liquidity pools on Ethereum.

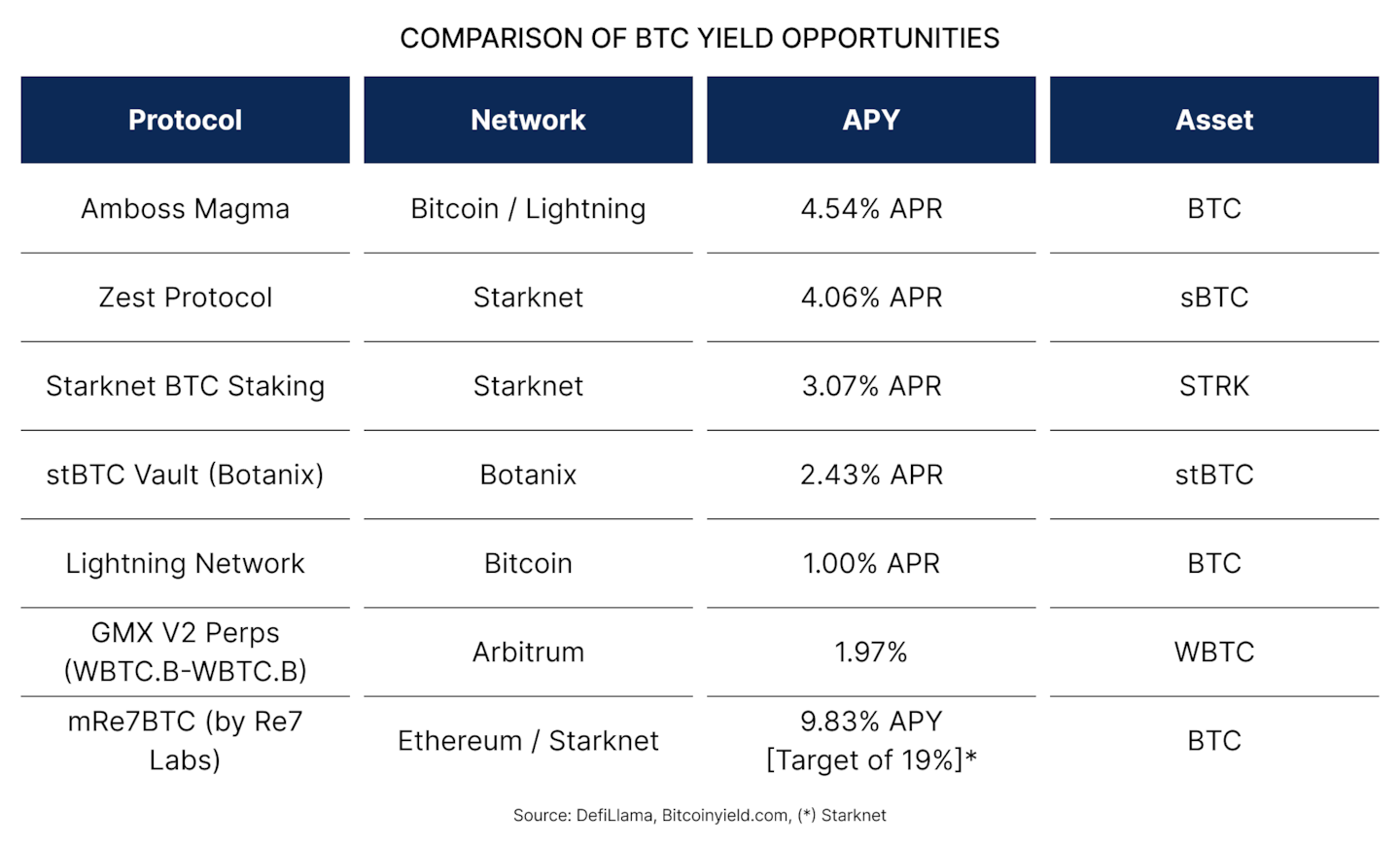

4 | Structured products

In addition to more DeFi-native yield-generation methods, such as staking, lending, and liquidity provision, more complex BTC-denominated strategies have also been deployed on Starknet.

Re7 is an asset manager with around $1 billion in assets under management. They run a BTC strategy that mixes systematic options trading off-chain with onchain elements. These include providing liquidity on Ekubo and staking Bitcoin on Starknet. You can access this strategy onchain through a tokenised product called mRe7BTC.

Currently, mRe7BTC offers one of the most competitive headline APYs among BTC-denominated yield products.

This competitiveness stems from the strategy’s additional components, such as systematic options trading and active positioning. It is not driven solely by passive, protocol-level yield.

It is also important to note that parts of the strategy operate off-chain. This introduces additional counterparty, operational, and transparency risks compared to fully onchain yield sources.

Starknet’s ability to onboard a product offering competitive APYs is impressive. The launch of mRe7BTC on Starknet is a positive sign. It shows that advanced institutional-level strategies can be built, deployed, and shared on Starknet’s infrastructure.

This suggests a level of ecosystem maturity beyond simple yield mechanisms. Moving forward, it’s crucial to watch how the strategy performs, especially as broader incentives on Starknet decrease and market conditions change.

Risks & Considerations

While it is clear that Starknet is making a serious push to become the BTCFi hub, four risks and considerations could limit its path to achieving that goal.

1 | Demand risk

BTCFi depends on institutional ownership continuing to grow. If we see a decline in institutional BTC holdings, whether through ETF outflows, corporates reducing balance sheet exposure, or a broader shift in allocations, the base that BTCFi can build on shrinks.

At the same time, regulation could turn more restrictive or infrastructure development could slow. Even if there is an intent to deploy BTC, institutions may be unable to participate if the infrastructure is not mature enough.

Finally, if interest rates decline meaningfully, the opportunity cost of holding idle BTC decreases. In that environment, the pressure to seek yield diminishes, weakening the core economic driver behind BTCFi.

2 | Incentive-driven liquidity

A large part of current yields on Starknet, especially in money markets and LP positions, comes from incentives. High APYs can attract liquidity quickly, but that liquidity might not stay if the incentives are not replaced by fees that keep APYs competitive.

If yields normalise and capital exits, Starknet could be viewed as an incentive-driven ecosystem rather than a strong BTCFi hub.

The key question is what happens to headline APYs as incentives decline and whether activity on Starknet can persist.

3 | Liquidity fragmentation

Supporting multiple BTC representations improves onboarding flexibility, but it also fragments liquidity and adds complexity. Depth can be diluted across pools, increasing slippage and operational friction.

That said, fragmentation may reflect the ecosystem’s early stage and could consolidate over time.

Whether Starknet can attract sufficient BTC liquidity across all of its BTC representations will ultimately determine whether it can overcome liquidity fragmentation and provide sufficient depth for institutional onboarding.

4 | Institutional adoption constraints

Institutional investors operate under strict custody rules, operational controls, and risk frameworks. Even with regulated custodians and account abstraction tools in place, adoption depends on whether BTC can be deployed without expanding established trust boundaries.

While infrastructure and regulatory clarity have improved, the ecosystem may still be too early for many institutions to take that step. Ultimately, time will determine whether both the infrastructure and the applications are mature enough to support meaningful participation.

BTCFi at Scale and Starknet’s Position

In our view, BTCFi will matter when institutional BTC holders see a real cost to keeping BTC idle. They also need the right setup to use BTC without losing custody and control.

As we approach 2026, these conditions are becoming clearer. About 14% of the BTC supply is already with institutions. What’s uncertain is whether these institutions think the current infrastructure is mature enough and whether interest rates will stay high enough to encourage them to seek yield.

A clearer signal that this inflexion point is materialising would be visible through several key indicators. These include sustained growth in BTCFi TVL across staking and lending markets, deeper BTC-denominated liquidity pools, and early participation from institutional holders such as corporates with BTC on their balance sheets or ETF providers beginning to explore yield generation on their holdings.

Starknet is already positioning itself for such a shift. The network is enabling BTC staking as part of its security model, launching a large BTCFi incentive program, and onboarding regulated custodians such as Anchorage. Together, these developments are building the infrastructure required for institutional BTC to move onchain.

From a competitive angle, Starknet offers attractive yields in staking, lending, and liquidity provision. Yet much of the yield advantage in money markets and LP pools still relies on incentives rather than organic demand alone. As these incentives fade, yields may decline unless borrowing and trading activity grow alongside liquidity.

This is where the real test starts. Starknet has made a strong, coordinated push into BTCFi and is ahead in preparation. The key will be whether today’s incentive-driven liquidity translates into lasting borrowing demand, steady trading activity, and genuine institutional interest. If it does, Starknet could become a leading BTCFi hub.