This spotlight is one of three sector deep-dives produced ahead of the upcoming State of RWAfi report, developed in collaboration with DefiLlama.

The full report delivers a comprehensive, data-led assessment of the real-world asset landscape across DeFi, covering tokenised equities, real estate, commodities, and the broader structural forces shaping the next phase of onchain capital markets.

The State of RWAfi Q1 2025 report will be published in the first week of April 2026.

Commodities are already financialised

Commodities are often framed as physical inputs to the global economy. In reality, they are deeply embedded in global financial markets.

The global commodity complex represents approximately $135 trillion in nominal market value, with oil and gas accounting for roughly 60% of that share and precious metals for around 30%. Here, “nominal value” refers to the aggregate notional exposure of financial contracts and traded instruments, not the physical stock itself. It reflects the scale of financial activity layered on top of real-world production.

Crucially, most investors never take delivery of oil barrels or gold bars. What they trade is exposure. Commodities today function less as raw goods and more as financial primitives within global capital markets.

Gold is the clearest example.

According to the World Gold Council, the physical financial gold market, including bars, coins, physically backed ETFs, and central bank reserves, is worth nearly $5 trillion. Gold is also one of the most liquid markets globally. WGC data shows average daily trading volumes of roughly $361 billion in 2025, rising to $623 billion in January 2026 before easing to $478 billion in February 2026, still well above 2025 levels. On top of this sits a large derivatives ecosystem across COMEX, LME, and OTC markets, used for hedging, macro positioning, and leverage.

Oil follows a similar pattern, though it is even more derivative-driven. Oil futures on CME and ICE generate enormous open interest and notional exposure, often running into the hundreds of billions of dollars globally. Oil ETFs such as USO and BNO manage billions in assets, providing simplified exposure without physical ownership. During stress periods, ETF positions have represented 5-10% or more of total oil futures open interest, illustrating how deeply financial and derivative layers are integrated.

Silver, while smaller than gold, is also heavily traded in financial markets. Futures contracts on COMEX and large silver ETFs represent billions of dollars in exposure. Like gold, silver is not just an industrial metal, it is actively used by investors as a financial asset.

Commodities therefore already serve as inflation hedges, reserve assets, portfolio diversifiers, collateral within structured finance and vehicles for macro positioning. In short, commodities are not pre-financial assets waiting to be digitised. They are already deeply financialised instruments.

Hence tokenisation does not invent their financial role. It proposes a new infrastructure layer for assets that are already liquid and represented through various financial instruments.

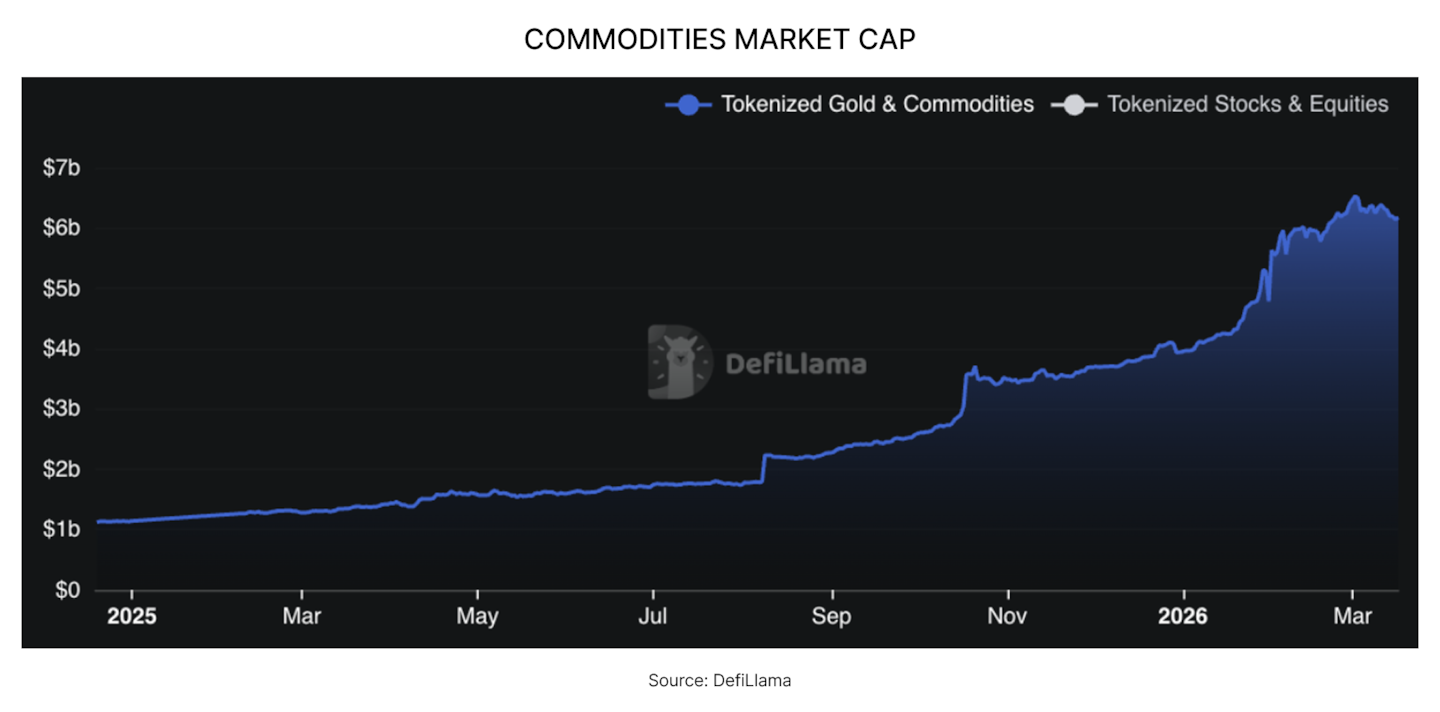

Since January 2025, tokenised commodities have grown from $1.1 billion to $6.4 billion, representing a 518% increase year-over-year. Gold dominates this market, representing roughly 95% of the total tokenised commodity market, led primarily by PAXG (~$2.4B) and XAUT (~$3.7B). Silver follows with a few hundred million dollars while tokenised copper, uranium or oil remain niche, often below $5 million in market capitalisation per asset.

Relative to a trillion-dollar traditional market, $6.4 billion remains marginal. Yet the speed of growth suggests something more structural than speculation. The question is whether tokenisation represents a temporary narrative cycle or the early phase of an infrastructure transition.

Why move commodities onchain

Commodities are not merely physical assets stored in vaults. They already trade as financial instruments through ETFs, futures, options and structured products. Tokenisation is therefore not about making commodities investable, that already exists. It is about upgrading the infrastructure that supports how these assets move, settle and interact with capital.

Today’s commodity markets are efficient at scale, but structurally layered. Physical allocation requires vaulting agreements, insurance coverage and custodial chains. ETFs rely on authorised participants and clearing systems. Derivatives depend on central clearing houses and margin frameworks. Settlement cycles, compliance procedures and cross-border frictions remain embedded in the system.

These mechanisms function effectively, but they are resource-intensive and primarily designed for institutional participants. Tokenisation restructures them to increase capital efficiency, expand accessibility and unlock composability.

First, settlement velocity.

Onchain assets settle in minutes rather than days. Ownership transfers are programmable and auditable without navigating multiple institutional intermediaries.

Second, capital accessibility.

Tokenisation lowers allocation thresholds. Exposure can be fractional and digitally transferable within regulatory constraints, expanding reach beyond traditional brokerage infrastructure.

Third, and more structurally, collateral mobility.

Commodities already function as collateral in traditional finance. But that collateral typically sits within custodial silos. A gold ETF share posted at one prime broker cannot frictionlessly circulate across institutions.

Onchain representation transforms commodities into portable collateral. A tokenised gold position can be posted, transferred, borrowed against or integrated into lending frameworks without replicating the full custody stack at each step. What’s emerging here isn’t incremental efficiency, but a new level of balance-sheet fluidity

Fourth, composability.

Once standardised as digital assets, commodities can interact with decentralised exchanges, lending markets and perpetual venues. This expands their functional range from passive holding instruments to active capital primitives.

Now the remaining question is whether all commodities migrate equally, or whether structural characteristics determine their trajectory.

The three structural models

Not all commodities behave the same. Structural characteristics such as stock-to-flow ratios, custody complexity, regulatory rigor and financial usage patterns shape how easily an asset transitions onchain. From these specificities, three categories emerge.

Monetary collateral commodities

Monetary collateral commodities are primarily held as stores of value rather than consumed. They possess high above-ground stock relative to annual production, are durable, divisible, fungible and globally recognised as reserve assets.

Gold and silver fall into this category.

Gold is the clearest monetary commodity. Above-ground stock vastly exceeds annual mine supply. It is held by central banks, ETFs, institutions and private investors as a reserve asset and inflation hedge. Price discovery is continuous and transparent and custody infrastructure is mature and standardised globally.

Silver shares similar properties but combines monetary allocation with industrial demand. Its price dynamics are more cyclical, yet structurally it remains storable and divisible.

Implication for tokenisation

These assets are structurally ideal for onchain representation. Indeed, custody is verifiable, units are standardised, price feeds are transparent and collateral logic is intuitive.

This explains why tokenised gold overwhelmingly dominates onchain commodity markets today. Its traditional role as monetary collateral translates naturally into programmable collateral onchain.

Strategic supply-constrained commodities

Strategic commodities derive significance from geopolitical positioning, energy security or technological dependency rather than monetary function.

Uranium is the clearest example.

Uranium is critical to nuclear energy and energy transition narratives. Supply is geographically concentrated and politically sensitive. Retail ownership of physical uranium is practically impossible. Exposure typically occurs through specialised funds or mining equities.

Unlike gold, uranium does not function as collateral. Its financialisation is constrained by regulation and oversight.

Implication for tokenisation.

Tokenisation here expands access rather than improving settlement efficiency. Adoption is likely to be institutional and permissioned rather than retail-driven or composability-first.

Industrial flow-based commodities

Industrial commodities are continuously produced and consumed within logistics-heavy supply chains. Their financial markets are dominated by derivatives used for hedging rather than long-term holding.

Oil and copper belong to this category.

Oil remains central to global energy systems. Copper underpins electrification and infrastructure. In both cases, futures markets dominate price discovery and financial exposure. Investors rarely seek physical ownership; exposure is synthetic via futures and swaps.

Implication for tokenisation

Onchain representation is more likely to emerge via perpetuals, synthetic indices or structured exposure rather than warehouse-backed tokens. Storage logistics, delivery mechanisms and margin structures complicate physical tokenisation.

A structural gradient

Across these categories, a clear gradient emerges that shapes the tokenisation market. As we move from gold to oil, custody becomes more complex, regulatory requirements increase, and financial behavior shifts from collateral holding to derivative hedging.

Gold leads because it is structurally simple to verify, store, and use as collateral. Silver follows due to similar properties. Uranium remains constrained by regulatory oversight, while copper and oil tend to migrate toward synthetic exposure.

The trajectory of tokenisation is driven less by narrative enthusiasm and more by structural characteristics.

Commodities are ready to expand onchain

Despite rapid growth, tokenised commodities remain small relative to their traditional counterparts. Yet several structural forces suggest continued expansion.

First, blockchain infrastructure has matured. Institutional-grade custody, compliance tooling and liquidity venues are now established. Ethereum accounts for approximately 75% of tokenised commodity issuance, followed by XRPLedger at roughly 15%, according to RWA.xyz, two ecosystems widely regarded as institutionally aligned.

Second, regulatory clarity around commodities is generally stronger than for other RWA. In the United States, physical commodities fall under the Commodity Futures Trading Commission framework rather than securities law, providing clearer classification boundaries. In Switzerland, commodities, particularly precious metals, benefit from long-established property and custody frameworks that facilitate structured tokenisation. In Singapore, the Monetary Authority of Singapore clearly distinguishes commodities from capital market products, reducing ambiguity in digital issuance. Within the European Union, commodities are recognised as distinct asset classes under MiFID II, with financial instruments referencing them regulated separately from the underlying physical assets. Compared to equity or real estate, commodities operate within more mature and clearly defined legal categories. Importantly, regulatory frameworks across jurisdictions show meaningful convergence in how commodities are classified and supervised, supporting cross-border issuance and trading.

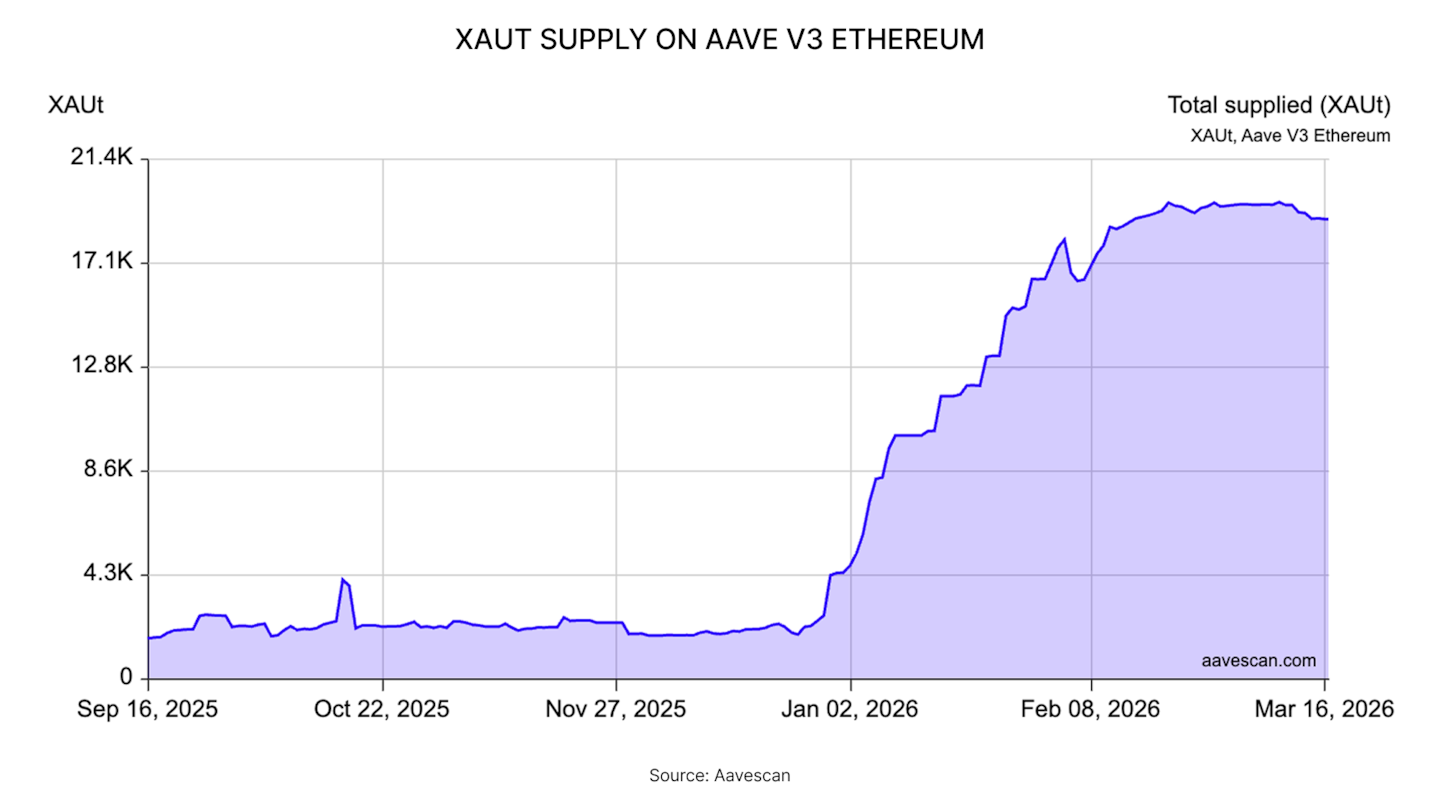

Third, the integration with DeFi is accelerating. The Aave XAUT vault expanded from roughly 1,900 XAUT to nearly 19,000 XAUT, a tenfold increase equivalent to about 900% growth in collateral usage. This trend illustrates how tokenised gold is increasingly used as productive collateral rather than sitting idle in wallets.

The recent launch of thGOLD, a yield-bearing gold representation issued by theo, provides another example of DeFi integration. Historically, generating yield on gold typically required accessing institutional lending markets with limited transparency and restricted access. Onchain, tokenised gold introduces greater transparency and flexibility: it can be posted as collateral, borrowed against, integrated into lending protocols, or embedded into structured strategies without relying on traditional custody infrastructure.

Overall, the conditions for commodity tokenisation are increasingly favourable, and the current momentum is unlikely to fade. Much like ETFs standardised access to commodities two decades ago, tokenisation represents the next structural upgrade, enhancing efficiency and embedding new financial layers directly into the asset itself.

If momentum persists, tokenised gold will likely remain the structural leader, with silver expanding alongside it. Other commodities will migrate onchain according to their inherent characteristics.

And as DeFi infrastructure continues to mature, commodities will transition from passive store-of-value instruments into active capital primitives onchain.

To understand in detail how commodities are growing onchain, how they are being used, how DeFi integration evolves, and what regulatory and risk considerations shape the trajectory, the full report provides a deeper analysis.

This spotlight is part of a three-part series examining the building blocks of the RWAfi landscape, produced ahead of the State of RWAfi Q1 2025 report with DefiLlama.