Tokenised stocks have quickly become one of the fastest-growing onchain asset classes. What was only a year ago a small market with roughly $30 million in active market cap has now expanded to more than $730 million.

Here, active market cap refers to the portion of a token’s total market capitalisation that excludes internal allocations such as treasury or team-held tokens, reflecting the value that is actually circulating in users’ hands onchain.

In a fast-paced market where many narratives are often short-lived, tokenised stocks have gained a strong foothold and continue to attract sustained interest.

This article explains what you need to know about this sector. We will cover why moving equities onchain matters, how tokenised stocks work, the current regulatory landscape, and how the market may evolve.

Why bring equities onchain?

Before we examine the architecture of tokenised stocks or the regulatory landscape, it is important to understand why we would want stocks to come onchain.

A 2025 World Economic Forum study on tokenisation lays out a clear, well-structured case for how tokenisation can deliver real user benefits. It does this by isolating five technical features that tokenised assets can introduce, then mapping each feature to a concrete value proposition and the associated risks.

The World Economic Forum’s framework is helpful because it cuts through the noise and focuses on what actually changes in practice with tokenisation.

When applied to tokenised stocks, the benefits become clearer. On the backend, there are efficiency gains from a shared system of record and greater programmability. For users, tokenised stocks can be integrated into DeFi applications, allowing investors to use their portfolios more flexibly, for example, as collateral or to generate yield.

It is, however, not just the WEF that came to this conclusion. The International Organisation of Securities Commissions (IOSCO) makes similar observations in its 2025 Final Report on Tokenisation of Financial Assets. Its report notes that shared and programmable ledgers can reduce reconciliation requirements, improve collateral mobility, and shorten settlement times. However, IOSCO also warns that the benefits observed to date remain modest and depend heavily on integration with existing regulated infrastructure.

Since many of the benefits outlined by the WEF and IOSCO are framed over a long-term timeframe and often still require further regulatory and infrastructure development, it can be useful to examine what is already in place and how it is already providing benefits to users.

xStocks, the tokenised equity standard launched by Backed Finance (Acquired by Kraken), is a great example of this.

With xStocks, users are already seeing tangible benefits, including 24/7 trading in and out of their stocks, easy ownership transfers, no broker commissions, DeFi use, and global access.

Given the benefits that tokenised stocks can bring to users and participants across the value chain, they represent the next step for financial markets. However, the larger structural benefits will take time to materialise.

Reducing reconciliation, automating corporate actions, enabling seamless cross-border settlement, and integrating with collateral and clearing systems all require regulatory clarity, infrastructure upgrades and coordination among market participants. The equity market is worth over $100 trillion, and expecting all of that value to move onchain quickly is unrealistic.

The good news is that while many benefits will take time, some are already clearly visible today. These immediate advantages are currently driving the growth of tokenised stocks onchain, with players such as xStocks and Ondo leading the charge.

Importantly, interest is also emerging at the exchange level: Nasdaq recently partnered with Kraken to explore enabling 24/7 trading of tokenised equities and ETFs, a signal that traditional market operators are beginning to seriously evaluate the infrastructure required to support tokenised financial assets

How tokenised stocks actually work

Over the past years, there have been many ways in which tokenised stocks have been launched, and the easiest way to distinguish among these approaches is through the lens of ownership. Some forms of tokenised stocks provide users with effectively zero real ownership and purely price exposure, such as synthetic tokens, whereas others can confer real entitlements or even direct shareholder status.

Currently, the market has largely moved away from earlier experiments with synthetic tokenised stocks, where no real stock was held in custody, and has shifted to custody-backed tokenised stocks.

In our upcoming RWAFi report, we examine each of these models in greater detail, but to understand how tokenised stocks work today, it is useful to focus on the custody-backed model that currently dominates the market.

The two largest issuers, which at the time of writing represent 99%+ of the tokenised equities currently actively onchain, are Backed Finance (now part of Kraken), the issuer behind xStocks, and Ondo Finance, which operates the Ondo Global Markets platform.

| Issuer | Active Market Cap (USD) | Market Share (%) |

|---|---|---|

| Backed Finance (Kraken) | $235,557,670 | 32.24% |

| Ondo Finance | $495,146,136 | 67.76% |

Both of these issuers operate under a custody-backed model. To better understand the model’s architecture, we will evaluate xStocks and its technical architecture, showcasing what is actually happening under the hood.

xStocks Architecture

When a new xStock is created, the process begins offchain with the purchase of a real share. A professional counterparty (either a qualified investor minting directly or an authorised participant that acts like a market maker) places an order for new xStocks and pays in fiat or stablecoins.

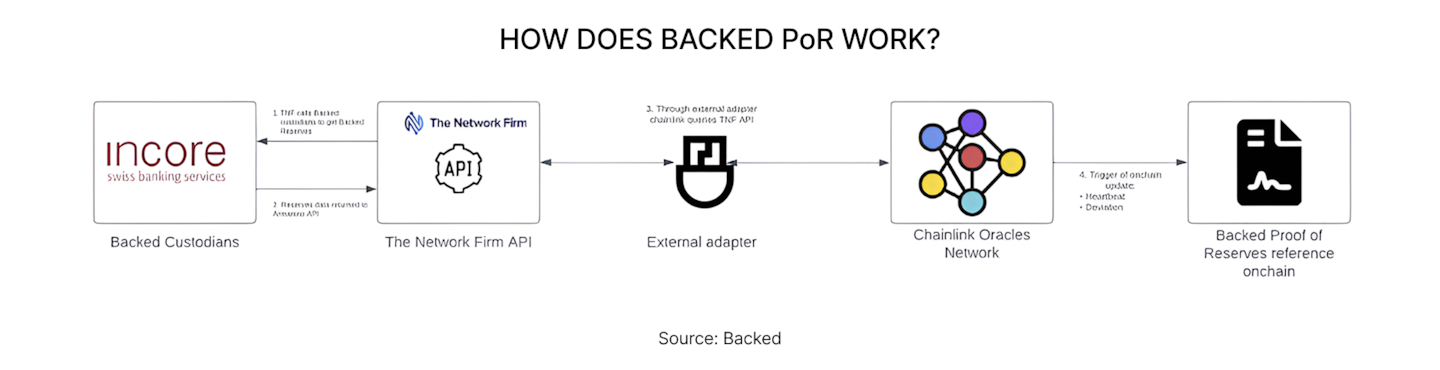

Backed Finance (now part of Kraken) then arranges for the underlying U.S. stock to be purchased through a regulated broker, such as Alpaca Securities LLC. Once the trade settles, the shares are held with regulated custodian banks in Switzerland, including InCore Bank AG and Maerki Baumann & Co. AG.

Custodying the assets is the most important step of the architecture. For every token that will later exist onchain, there must first be a real share sitting in custody. The structure is set up so that a dedicated issuing vehicle holds the rights to those shares, and legal service providers are involved to formalise the claim on the underlying assets.

KYC is also built into the issuance layer. Authorised participants (APs) who mint or redeem tokens directly with the issuer must complete regulated onboarding and compliance checks before any funds are accepted or shares are issued.

This means the primary entry and exit points of supply are fully controlled and compliant.

Once the tokens are circulating onchain, secondary trading rules depend on the specific venue and jurisdiction.

The onchain process begins only after the underlying shares have been secured. Backed Finance then issues a corresponding token on public blockchains such as Solana, Ethereum and BNB Chain. Each token represents exposure to a specific stock and is minted only if a matching share is already held in custody. If tokens are later redeemed, they are burned, so the number of tokens in circulation remains aligned with the number of real shares backing them.

To give users confidence that this backing actually exists, Backed uses a proof-of-reserves setup. An independent auditor verifies the custody accounts and confirms that the shares are there. That information is then published onchain through Chainlink, allowing anyone to check that the token supply matches the underlying assets. Updates occur at least once per day, more frequently as needed.

For the user, interaction with xStocks begins only after the tokens are minted. They can then trade them on centralised exchanges such as Kraken or Bybit. At the same time, because these tokens are onchain they can also be withdrawn to a self-custody wallet and used in DeFi. On Solana, for example, users can provide liquidity on Raydium, swap via Jupiter, or supply the tokens to earn a yield in a lending market like Kamino.

Chainlink plays an important role in making products like xStocks function reliably onchain. Its price feeds ensure that decentralised markets reference accurate and tamper-resistant market data. In addition, Chainlink provides dedicated data feeds for corporate actions, including dividends and stock splits.

In the current xStocks design, dividends are automatically reinvested into token balances, so users do not need to take any manual action. This is similar to how many traditional brokers offer automatic dividend reinvestment plans, where payouts are used to buy additional shares rather than being paid out in cash.

On top of that, Chainlink’s cross-chain messaging system, CCIP, also helps maintain consistency when tokens move between different blockchains. Together, these services demonstrate that oracle infrastructure is a key building block for enabling tokenised stocks to operate smoothly across blockchains.

Seen as a whole, this model shows how far tokenised equities have already come. It connects regulated market infrastructure with public blockchains in a way that actually works in practice.

The limits of the custody-backed model

It is clear that xStocks and other custody-backed models like Ondo Finance represent a major improvement over earlier tokenised stock models. In the past, many platforms offered synthetic tokens or derivatives that did not represent any real shares.

These models were typically backed by pooled crypto collateral and relied on overcollateralisation and active risk management, meaning users were exposed to collateral shortfalls, liquidation risk, and the solvency of the protocol rather than having a claim on actual underlying equity.

The custody-backed model used by xStocks is much stronger because real shares are actually purchased and held with regulated custodians.

However, it still has limitations, as users’ actual ownership is quite limited. In this model, the token is a contractual claim against an issuer or SPV, not direct ownership of the underlying shares.

With a model like this, 5 key limitations emerge that users should be aware of.

- You are not directly registered as a shareholder on the company’s books.

- Because the holder owns a note or contractual claim rather than the share itself, voting rights and other shareholder privileges are typically not directly available.

- Your claim depends on the issuer structure, custody arrangements, and legal documentation.

- Redemption into the underlying shares may be restricted to authorised participants, subject to minimum sizes, fees, or operational conditions.

- The structure spans multiple entities, jurisdictions, banks, brokers, and service providers. While regulated, this adds legal and operational layers between the token holder and the underlying asset.

To fully address these limitations, issuers would need to move toward either a tokenised entitlement model or shares that are directly registered onchain.

Is regulation slowing the market’s progress?

A lot has been happening around the regulation of tokenised stocks. While much remains unclear about how they will ultimately be treated across jurisdictions, one point most regulators now agree on is that tokenised equities remain securities. Tokenisation is largely viewed as a change in the record-keeping and transfer layer rather than a way around securities law.

In the United States, this position was reinforced in January 2026, when the SEC’s Division of Corporation Finance, Division of Investment Management, and Division of Trading and Markets issued a joint staff statement on tokenised securities. The statement did not create new rules. Instead, it was directed to issuers and was intended to reinforce that existing federal securities laws will also apply to tokenised stocks.

This posture helps explain why the custody-backed model has become the dominant design. It fits most cleanly inside today’s regulated perimeter. The underlying shares can be purchased through regulated brokers and held with regulated custodians, while the onchain token is distributed.

What has improved

One of the most important developments in 2026 is that, rather than just crypto-native companies working on tokenised stocks, we are seeing industry giants enter the field, with the DTCC and the New York Stock Exchange as two of the clearest examples.

SEC green lights stock tokenisation via DTCC

In December 2025, DTCC and its subsidiary, The Depository Trust Company (DTC), received an SEC no-action letter authorising them to proceed with a tokenisation service for certain assets held at DTC.

A broader rollout is expected in the second half of 2026, with reports suggesting that DTC is exploring plans to allow a subset of U.S. Treasury securities it holds in custody to be minted onto the Canton Network, a public blockchain built specifically for RWAs. If the initial phase proves successful, the model could later expand to additional asset classes.

To understand why this matters, it helps to know what DTC is. DTCC sits at the core of the US capital markets infrastructure. Through DTC, it holds and settles the vast majority of US equities and many other securities.

The no-action letter from the SEC signals that the SEC staff would not recommend enforcement if DTC proceeds with its plan to launch its tokenisation platform in 2026. That provides important regulatory assurance and demonstrates there is room for innovation.

The programme is expected to begin with large U.S. stocks, including the top 1000, Treasuries, and major ETFs, with tokenisation occurring at the request of DTC members.

It should also not be overlooked that the DTCs plan to tokenise stocks focuses on tokenised entitlements and is designed to provide investors with stronger ownership rights than the custody-backed model discussed earlier. The token is structured to carry the same rights and protections as the traditional security, which is a step in the right direction.

NYSE announces tokenised securities platform

Shortly after the DTCC announcement, the New York Stock Exchange, part of Intercontinental Exchange (ICE), introduced its own plan for a tokenised securities platform. While DTCC focused on tokenised entitlements within existing post-trade infrastructure, the NYSE proposal moves one layer higher in the stack. It targets the trading venue itself.

The NYSE is developing a new digital platform that would enable 24/7 trading of tokenised US equities and ETFs, support fractional share trading, and enable immediate settlement with stablecoins. The platform is still subject to regulatory approval, but this would power a new NYSE venue where tokenised shares are fungible with traditionally issued securities, meaning they represent the same type of exposure and shareholder rights, including dividends and governance.

Architecturally, the model separates trading from settlement in a familiar but upgraded way. Orders would still be matched using the NYSE’s existing Pillar matching engine, which is the same core technology used in today’s markets. The difference comes after the trade. Instead of relying solely on traditional clearing and settlement rails, the post-trade layer would integrate blockchain-based systems to enable onchain settlement and token movement.

In practice, that means three things change. First, trading could run 24/7 rather than during fixed market hours. Second, funding could be provided via stablecoins or tokenised deposits, allowing capital to move outside traditional banking hours. Third, instead of trades being finalised the next business day as they are today, the transfer of money and ownership could be completed almost immediately.

ICE has also signalled that it is preparing its clearing infrastructure to support continuous trading and tokenised collateral, working with major banks to enable tokenised deposits across its clearinghouses.

Nasdaq partners with Kraken to offer tokenised stock trading

More recently, Nasdaq has also announced a partnership with Kraken’s parent company Payward to support the development of infrastructure for tokenised equities. The collaboration builds on Nasdaq’s earlier tokenisation proposal filed with the SEC in September 2025 and aims to connect regulated equity markets with blockchain-based financial networks.

Under the arrangement, Payward will work with Nasdaq to develop an equities transformation gateway that links traditional capital market infrastructure with blockchains. The system will use Kraken’s xStocks framework to allow blockchain-based representations of publicly traded shares to be issued.

Within this architecture, Nasdaq’s issuer-sponsored equity tokens would remain anchored within regulated market infrastructure, while the xStocks framework supports the permissionless side of the ecosystem. Kraken will also act as a distribution partner, enabling eligible customers outside the United States to access tokenised versions of public company shares through its platform.

Nasdaq expects its equity token framework and related distributed ledger services to begin rolling out in the first half of 2027. Together with the DTCC and NYSE initiatives, the partnership shows how tokenised securities are starting to move into the core infrastructure of global capital markets rather than remaining limited to crypto native platforms.

What is still holding innovation back

Even with this momentum, we remain far from a clear, globally consistent regulatory framework for tokenised stocks. That uncertainty is one of the main reasons the market is still dominated by custody-backed wrappers.

The first challenge is simple fragmentation.

A tokenised equity can be treated very differently depending on the user’s location. As a result, leading issuers rely on strict eligibility checks and geo-restrictions. You can already see this with products like xStocks, where access is limited for US users on exchanges such as Kraken. If tokenised stocks are to reach mass adoption, clearer, more harmonised rules across jurisdictions will be necessary.

The second challenge is where these assets are allowed to operate.

Regulators are generally comfortable when tokenised equities remain in supervised custody and are distributed through controlled channels. They become far more cautious when those same assets move into open, permissionless venues and are used in DeFi in ways that could create a parallel market for the same underlying equities.

This is also why initiatives like DTCC and the NYSE are expected to begin in permissioned environments. They are designing infrastructure for regulated broker-dealers and supervised participants. That approach fits within today’s regulatory expectations.

The tension appears when tokenised stocks leave that controlled setting. Issuing a tokenised equity within a permissioned framework is one thing. Another is having that token actively participate in DeFi and trade on DEXs.

So the real question is not whether tokenised stocks will continue to grow. They already are. The more important question is whether regulation will eventually create space for permissionless tokenised equities to expand, or whether the market will split into two distinct tracks, with large-scale growth happening inside permissioned systems while open DeFi use remains constrained. As long as regulators do not clearly address this question, a grey area will remain.