Real estate is the largest asset class in the world, valued at more than $380 trillion. Yet the way it is transacted remains largely analogue. Deals depend on paperwork, manual checks, government laws and many intermediaries and approvals.

Ownership is recorded in national land registries and validated through notarial systems. Each transfer passes through multiple layers of verification, which adds time and expense. Cross-border investment is even more complex. Every jurisdiction applies its own property law, tax rules, and compliance standards. Allocating capital internationally therefore requires legal structuring and specialised intermediaries.

Real estate is also difficult to divide. Fractional participation usually requires SPVs, trusts, or fund vehicles. These structures introduce governance layers and higher minimum investments, concentrating capital in institutional channels. Limited secondary markets further extend holding periods, as exiting a position can be slow and costly.

Tokenisation enters as an infrastructure upgrade.

The objective is not to replace property law, but to digitise elements of issuance, ownership tracking, income distribution, and transfer logic. If economic rights can be expressed in programmable form, settlement can accelerate, reporting can become more transparent, and fractional participation can scale more efficiently.

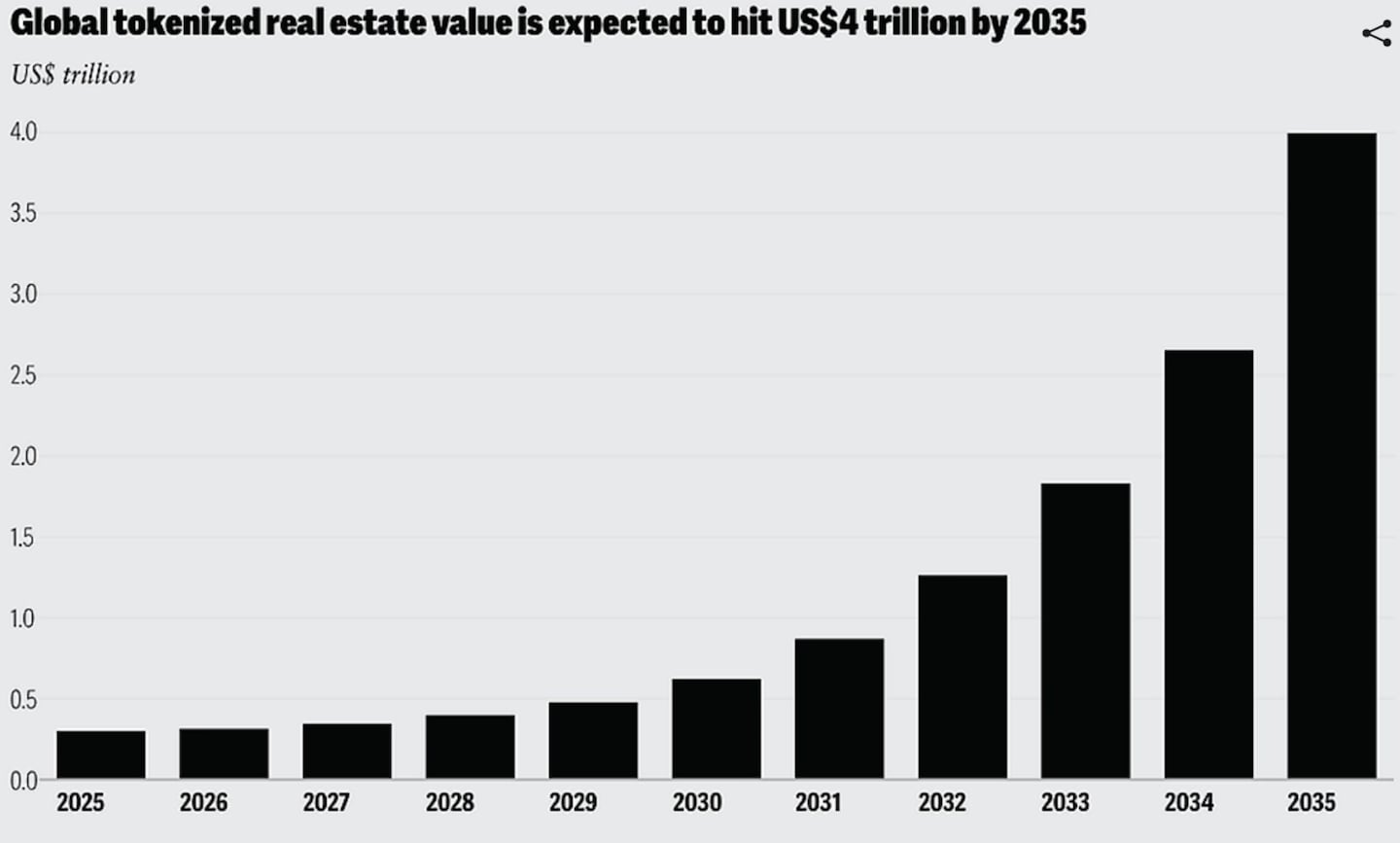

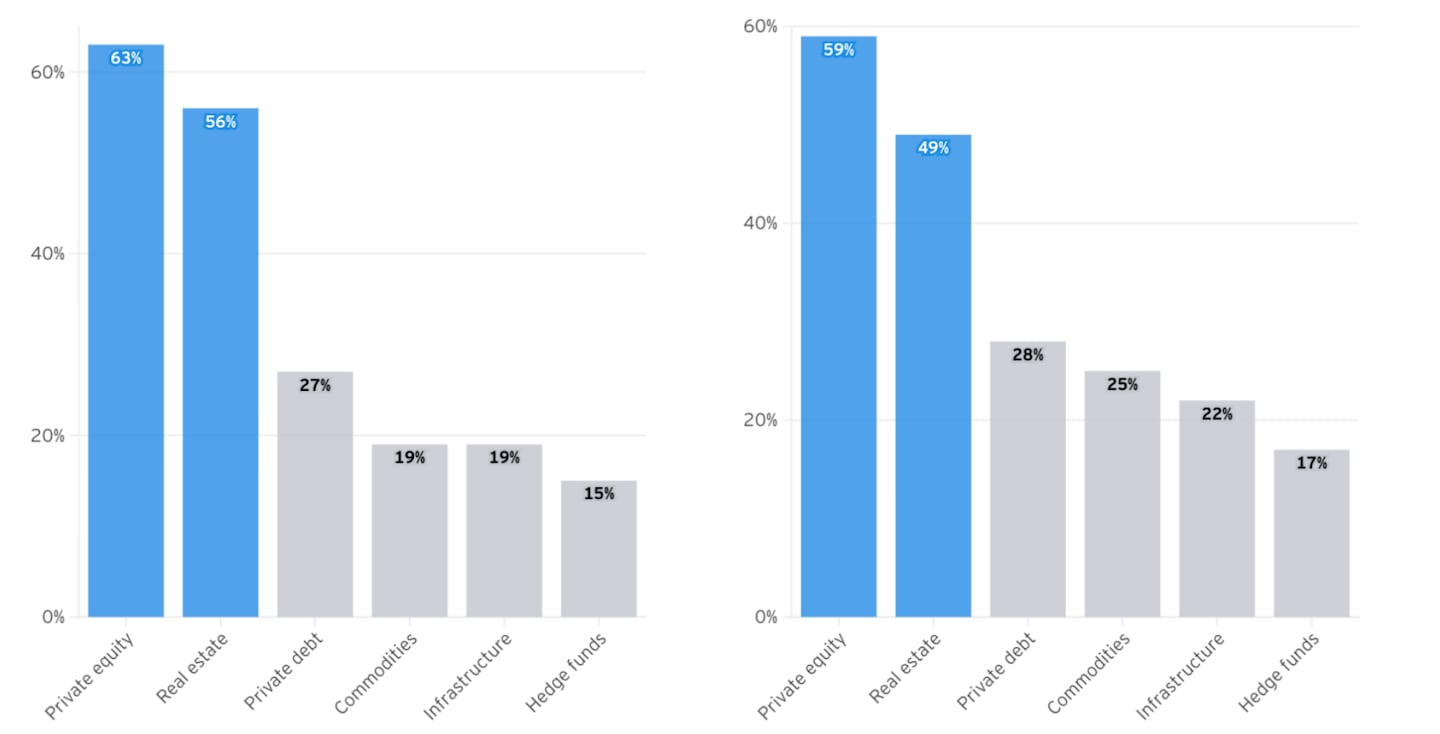

Market projections reflect this structural momentum. Deloitte estimates that several trillion dollars of real-world assets could be tokenised over the coming decade, with projected growth rates around 27% CAGR. Institutional surveys from EY and others reinforce this interest, with 49% of high-net-worth investors and 56% of institutional investors ranking real estate among their most attractive tokenised asset categories.

Looking at the present state, tokenised real estate is no longer theoretical. Pilot programmes, regulated offerings, and protocol-level initiatives are active across multiple jurisdictions. Combining data from DeFiLlama and RWA.xyz suggests a current onchain market size in the range of $500/600 million. The true figure is likely higher, given differences in classification, private placements, and limited public disclosure by certain issuers.

Tokenisation is not only about putting buildings on a blockchain but about restructuring how rights, capital, and administrative processes around real estate are coordinated. This article explores why real estate is moving onchain, how the technology enables it, and the four structural models through which tokenised real estate is implemented today.

Why move real estate onchain

Within this context, tokenisation addresses the structural frictions in how real estate is issued and managed. The core drivers are outlined below:

Transparency.

Onchain records provide timestamped transaction histories and distribution logs. While legal title remains in national registries, the operational layer becomes more traceable and standardised.

Capital efficiency.

Issuers can streamline fundraising and post-issuance servicing. Investors may benefit from simplified administration and potentially improved liquidity compared to traditional private placements.

Fractionalisation.

High property values create barriers to entry. Tokenisation divides economic interests into smaller units, lowering minimum tickets and expanding distribution beyond local or institutional investor bases.

Settlement efficiency and cost reduction.

For investment vehicles, smart contracts can automate yield distribution, bookkeeping, and ownership tracking. This reduces manual processing and reliance on multiple service providers. Compliance and legal layers still apply, but greater operational efficiency can improve margins, increase competitiveness, or generate savings at scale.

For public administration, integrating blockchain into registries and settlement workflows can reduce duplication, paperwork, and coordination between notaries, registrars, and government departments. While property law and oversight remain unchanged, operational processes can become faster and less resource-intensive.

Security and record integrity.

Distributed ledgers provide tamper-resistant records of issuance and transfers. While legal ownership remains anchored in national registries, the operational layer benefits from immutable audit trails. This reduces reconciliation disputes, improves data integrity, and strengthens trust between issuers, administrators, and investors.

Interoperability potential and DeFi Composability.

Once real estate exposure exists in a tokenised form, it can interact with digital financial infrastructure. Portfolio reporting, automated compliance systems, structured lending frameworks, and risk management tools can integrate more easily with standardised onchain representations. Even if full DeFi integration remains constrained by regulation, the technical foundation enables future interoperability.

How tokenised real estate works in practice

Unlike tokenised treasuries or stablecoins, real estate is anchored in territorial law. Property rights are jurisdiction-specific, non-fungible, and embedded in administrative systems. This makes real estate structurally harder to standardise across borders but not inherently complex from a technical perspective.

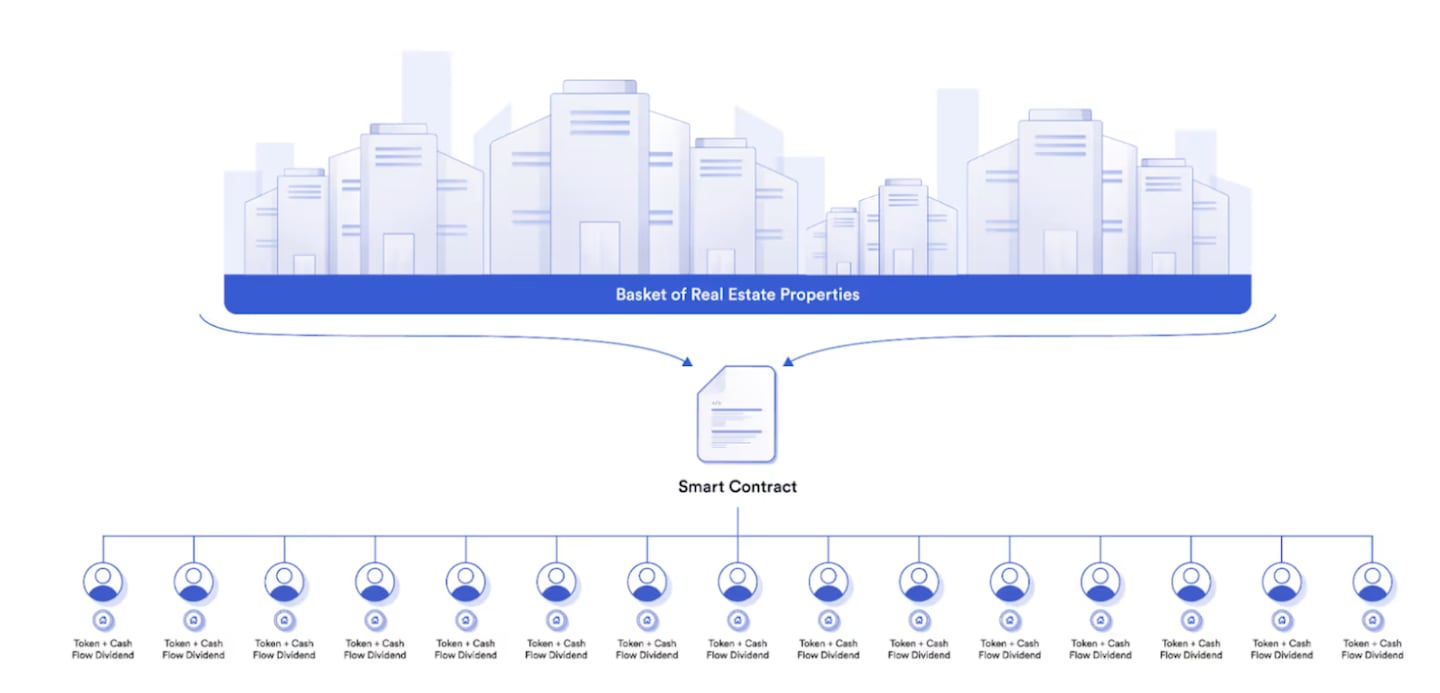

A property can be represented as an NFT when uniqueness matters, or as fungible tokens when fractional ownership or economic exposure is divided into standardised units. In many cases, the asset itself is not placed directly onchain. Instead, a tokenised SPV, fund unit, debt instrument, or ETF-like vehicle represents the economic rights linked to property held by a legal entity.

Transfer logic can be permissioned or open, depending on regulatory constraints. Compliance checks, wallet whitelisting, yield distribution rules, issuance caps, and transfer restrictions can all be embedded directly into the token contract.

The real technical challenge lies in coordinating onchain execution with offchain legal and economic reality. Three elements are critical:

Legal structuring.

Before any token is issued, a legal framework must define what it represents. It may correspond to equity in a property-holding entity, a debt claim, a revenue participation agreement, or another enforceable right. Without this mapping, the token has no economic meaning. Smart contracts express execution logic, but enforceability remains grounded in corporate and property law.

Asset verification and data inputs.

Real estate does not trade continuously on transparent markets. Valuations depend on appraisals, rental income, and regional benchmarks. Integrating these assets into digital systems requires trusted data sources. Reliable oracle infrastructure becomes essential, particularly when tokens interact with lending or collateral frameworks.

Custody and compliance infrastructure.

Investor onboarding typically involves KYC, AML, and jurisdictional eligibility checks. These processes often occur offchain but are enforced onchain through transfer restrictions or wallet whitelisting. The token reflects compliance constraints rather than bypassing them.

In practice, growth in tokenised real estate depends less on smart contract innovation and more on alignment between legal systems, financial intermediaries, regulators, and digital infrastructure. In other words, the limiting factor is the institutional integration and not blockchain capability.

The four models of tokenised real estate

Tokenised real estate is often discussed as a single concept. In reality, it operates through four distinct structural models, each representing a different way of expressing property rights or economic exposure onchain, often shaped by jurisdictional constraints.

Onchain representation of property data

The first model does not tokenise ownership at all. Instead, it places selected property data onchain while legal title remains fully governed by traditional land registries.

Blockchain is used to record elements such as ownership history, valuation updates, energy certificates, maintenance logs, or notarised documentation. The chain acts as an audit and coordination layer, improving transparency and tracking. The objective here is infrastructure modernisation rather than financial innovation.

Direct or fractionalised ownership

The second model seeks to move ownership itself onchain. In its pure form, the token would represent legal title to the property, either for a single owner or fragmented across multiple holders. In such a configuration, the notarial and transfer process would effectively be digitised.

Technically, this is feasible but, legally, it remains complex. Most jurisdictions do not yet recognise blockchain tokens as valid instruments for transferring property title. Pilot programmes are emerging, and deeper integration with land registries could eventually transform how real estate is settled and traded. However, significant constraints persist: liability allocation, governance rules, tax treatment, and AML compliance frameworks must all align with property law.

This model is closest to the intuitive idea of “owning property onchain”.

Financial wrappers

The third model is by far the most dominant today. Instead of tokenising the property directly, it tokenises a financial instrument linked to the property.

Investors purchase tokens representing equity or debt claims issued by an entity that owns or finances the asset. The property sits inside a legal wrapper, and the token reflects rights against that entity. These structures take several common forms:

- SPV equity: A Special Purpose Vehicle acquires the property. Tokens represent shares in that vehicle, entitling holders to rental income and potential liquidation proceeds.

- Tokenised debt: Investors fund projects through participatory loans or structured debt instruments. Returns are contractual rather than ownership-based.

- Trust or yield vehicles: Exposure may be tied to real estate-backed debt positions rather than direct asset participation.

- Portfolio tokens: Tokens provide diversified exposure to multiple properties, similar to a real estate ETF structure.

Because these models align with existing corporate, fund, and securities law, they scale more easily. They offer regulatory clarity and operational feasibility. However, they also introduce entity risk, counterparty exposure, and insolvency considerations. In this configuration, the token is effectively a digital wrapper around a traditional financial structure.

Synthetic and derivative exposure

The fourth model does not tokenise property at all. Instead, it tokenises exposure to real estate-related metrics. For example, platforms can create perpetual contracts or prediction markets referencing square metre prices in specific regions, or structured instruments tracking property indices.

These products serve as hedges, speculative tools, or price discovery mechanisms. They behave more like financial derivatives than real estate investments. There is no claim on rent, no legal ownership, only financial exposure.

The structural constraint

Taking a step back, a clear asymmetry emerges between technological readiness and institutional readiness.

On the one hand, the technology is ready. Smart contracts, token standards, and oracle infrastructure can embed yield distribution, compliance rules, transfer restrictions, reporting logic, and even selective composability with DeFi. From a purely digital standpoint, there is no structural barrier preventing real estate from existing onchain.

On the other hand, adoption is defined by institutions and regulation. Legal systems determine the boundaries within which tokenised real estate can operate. While blockchain can modernise settlement, reduce administrative costs, and digitise notarial processes, regulatory change takes time to be recognised, coordinated, and implemented.

This asymmetry is particularly striking for the ones who have been following the sector for years. In 2020, many governments and institutions argued that blockchain infrastructure was not mature enough to support real-world assets. Today, the situation has reversed.

This difference in velocity also explains the current market structure. As explored in greater depth in the full report, SPV-based tokenisation dominates because it fits within existing securities and corporate frameworks. It enables scale without rewriting property law. Yet it remains a financial wrapper around real estate rather than direct onchain ownership.

The deeper transformation, one that would bring investors closer to the idea of truly “owning property onchain”, lies in registry integration and title digitisation. Pilot initiatives, such as those emerging in Dubai, point in this direction. If land registries and notarial processes become digitally native, real estate could gain structural transparency, faster settlement, and materially improved efficiency at the infrastructure level.

For now, tokenised real estate sits between two worlds: technologically ready, yet institutionally constrained.

To understand how jurisdictions are shaping this evolution, how regulation defines what is permissible, and how real estate is actually used onchain today, the full report provides a more in-depth examination.